Portfolio Update - November 22 Edition

State of play and a few "Thank Yous"

Disclaimer: Nothing in this post is investment advice. The author owns all the securities listed in the table below. His views may be biased, he may buy or sell any security mentioned atany time. The information posted is not to be relied upon. Please do your own research.

Even thought this is not the end of a quarter or month, I am posting this update just in the middle of a quarter to describe where the portfolio stands and give a few updates. I am somehow struggling to balance shorter overview updates with “deep dives” on the substack. While I personally think, the deep-dives are more valuable, short updates or a trading log appear to be better received by many readers. So after fairly detailed pieces on Sixt and Autohellas, here comes an overview again. there have been some changes which are worth discussing.

In terms of performance, the portfolio, which my partners and me started this years is up about 3.5% on the capital invested so far - that is on a EUR basis. There have been two drawdowns of capital in March and June and I am expecting the final one to happen in December, We should then have a stable capital base for next year. While I am satisfied with the performance, I want to make it very clear that a performance over a few months is clearly not statistically significant and says nothing about an investor’s skill. I think you need to look at a track record of at least five years for that. Also, note that I will not spend any time on this blog to discuss the definition of a benchmark. While I look at indices and will mention them from time to time, I will not take part in what Seth Klarman wisely aptly called the “relative performance derby”. Some institutionaly might have to run there - I do not.

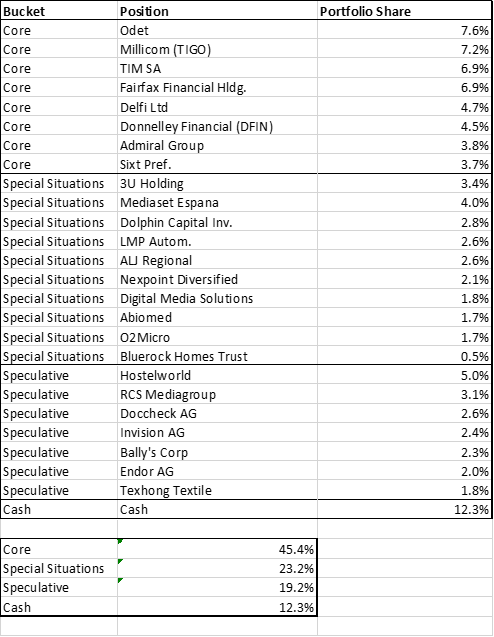

With the opening remarks out of the way, let’s jump in. Here is the current state of play. If you like, compare it to the latest update from late August.

What has changed?

In the core bucket, I sold my Fuchs Petrolub position. While I still very much respect the company and the latest results looked decent superficially given the difficult evironment they operate in, I remain concerned with their cash generation. Pretty much their entire earnings have had to be reinvested into Working Capital. This will not need to be the case forever, still I do not really like it and so exited at a small gain (purchased @23.50, sold @25.25)

Also, I reclassified Delfi from a “speculative” to a “Core” holding. While it cannot really be seen in the stock price, my favourite Indonesian chocolate producer has achieved stellar results so far in 2022 and is on track for the best revenues and profit margins in the last seven years, coupled with a return on equiy >15%. You can still buy Delfi at 4xEBITDA / 5x EBIT which strikes me as - well - pretty darn cheap. I am more confident than ever in the future of the company. While I have not written up Delfi, there is plenty of only analysis available - for example Michael Fritzell has covered it really well.

On to Special Situations:

I took a big victory lapon Twitter and a smaller one on Citrix, both of which closed. While Twitter was a smallish position, it provided a great learning experience for me as there was a great network of investors changing views on - yes, Twitter - and also a fantastic coverage on the Yet Another Value Podcast by Andrew Walker, providing high-grade information. Also, playing the merger thesis inpart via options (Call Spreads) was something I had not done before and which worked well in this instance.

Other exits in the special situations bucket include Exmar and Swedish Match. Exmar was in idea pitched here on Valueandopportunity . The company had made a major asset sale and a big dividend was to be expected. While the sale closed as expected and the stock performed quite well, I was also getting less confident on the dividend after their latest reporting. Given the reduced upside after the share price run-up, I took my modest gains (bought @ 8.55 , sold @10.22) off the table here (like Valueandopportunity his slightly larger gains). Another example how it pays to read good investment blogs.

On the Swedish Match takeover by Philip Morris International, a price recut ocurred as anticipated yet it was of a disappointing magnitude (106 to 116 SEK/share). After the recut was published I sold my shares quite quickly as I was unsure whether Elliott and Bronte would accept the deal at this price (they did). Had it fallen thorugh, the Swedish Match shares might have fallen quite a lot. I therefore sold my shares around 113 SEK/share. The situation remains very interesting since (1) PMI is now in a very interesting spot of being the global leader in non-smoke nicotine products (they now own the IQOS and ZYN brands) and (2) Swedish Match, which still trades on the market, might be squeezed out (any experts in Swedish Squeeze Outs reading this?)

What is new in special situations? Abiomed and O2Micro should hopefully two fairly straightforward merger arb situations. Abiomed includes a CVR and should close this year while O2Micro is one for next year. I have looked at some more controversial mergers like Activision/Microsoft or Silicon Motion/MaxLinear but not yet been comfortable to invest.

I personally think that Dolphin Capital Investors has an interesting setup. The company has been a trainwreck for years and so far only burned capital for its shareholders. It is however in clear liquidation mode now, has recently sold one of its three meaningful assets, hoping to divest the second one still this year. It has also seen some modest insider buying recently. So I am still bagholding here.

Other new positions include 3U Holding (another thanks to ValueandOpportunity ! ) and Mediaset Espana. I learned of Mediaset Espana on Twitter and it has run up a bit since I invested, but the setup is still compelling. 83% of the company is owned by MediaforEurope (Berlusconi). In June, MediaforEurope tendered for more shares at a price of 4.32 EUR a share in a cash/stock combination deal. In the meantime Mediaset Espana trades at 3.14 EUR/share (and below 2.50 EUR recently). They generate 60 Cents/Share in earnings, hold net Cash of about 1 EUR a share. They also own 11.46% in ProSiebenSat1 Media (worth another 0.75 a share at current prices). So this again looks really cheap, yet there is a risk of Berlusconi playing some dirty tricks / disrespecting minorities. We will see how this play out.

On the speculative bucket, not too much has changed. Maybe worth mentioning that I now own a trio of German technology hopefuls (Blame my home bias): Doccheck, Invision and Endor. I consider each of the three high risk, but also high potential return. Doccheck (formerly Antwerpes AG) runs an interesting platform of services for the health sector, including a marketing agency for pharma/health products, a professional social network for medical professionals and an online distribution oof pharma products. Each of these can be interesting niches and the product distribution segment had massive one-off gains due to Covid products in the last two years. While these were extraodinary, I believe that thesecular trends for Doccheck might also be decent. Like Endor and Invision, Doccheck is owner-operated. It is conservatively financed and trades fairly cheaply if you expect some overall growth.

Invision is a more difficult case if you purely look at its numbers. The company is currently in a spending phase, hiring staff for its ongoing rollout of Injixo, a SaaS product for Workforce Management ( a main application is Call Centers). At the moment, the company is growing its Recurring Revenue Basis for the SaaS product but, given the cost build-up, burning cash to get there. Invision were targeting revenues of EUR 50mm and an EBIT marginof 25% by 2025. While this looks optimistic to me, even if they reach this one or two years later, returns should be quite goog, given the market cap stands at 29mm EUR right now. With all the SaaS carnage, and the company having mentioned that it may potentially ask for a capital increase, Invision trades at long-term lows at the moment. So, this is a risky proposal, but also a potential multibagger from here. If you want to read more on Invision, the best source are letters from TGV Rubicon.

Finally, Endor is a leading provider of Simracing equipment (wheels, pedals, gear, brakes). While I am not active here, this has been a growing market and Endor seems to be the leading supplier completely focused on the segment (through the Fanatec brand). Competitors are more diversified companies like Logitec and from what I have heard, Fanatec offers good quality and is respected in the community. While revenues can be lumpy and geared to game releases (Gran Turismo 3 helped them a lot this year), I would expect for the market to grow over time. Endor has a market cap of 200mm EUR, little debt and generated 17mm EUR in EBIT for H1 2022. Surprisingly, for a small company which is only trading at Munich Regional Exchange, it has been written up twice on VIC and covered on Yet Another Value Podcast .

That’s the quick roundtrip through the portfolio. I am still pretty sceptical of the overall market recovery. Given the rate shifts and recession risk, I think stocks overall are trading too high at the moment. On the other hand, it feels good that some of the most obvious bubbles (crypto, SPACs, unprofitable tech) have deflated. Yet, many stock prices have recovered, implied volatility has come down a lot and a generally optimistic moods has returned. Call me a pessimist, but I do not trust the swings yet. As a long-only investor, I feel comfortable holding some cash and non-correlated positions in order to be dressed well, should the tide go out.

As usual, comments / feedback / questions / criticism are highly appreciated.

Good performance and great overview. Many thanks!

How do you think about working capital build ups in detail? Would it be alright, if the build up didn't consume the entire free cashflow?

Once working capital normalizes a bunch of companies will get +10% of their enterprise value as cash inflow. A recession might even increase the cash inflow while share prices should fall. This could be a big value driver with the right capital allocation policy.

I'm starting to actively look for such companies now. I guess chemical companies like Fuchs Petrolub and distribution companies like Ferguson fit description.