Car Rental Companies (2)

The secret sauce of Sixt

Disclaimer: This is not investment advice. The author owns Sixt Pref Shares long and may buy or sell at any time. The information provided may be inaccurate and the views biased. Please do not rely on this report for investment decisions and do your own research.

After Covid knocked me off for a couple of days, I present, later than expected, the second part on the two car rental companies which I am invested in ( Part One with a focus on Greek Autohellas is here ).

Based in in Pullach near Munich, Sixt has been a household name for Germans for many years. The company is famous for its funny-to-sarcastic ads featuring celebrities (mostly politicians) and therefore has a certain share of mind at least in Germany.

A selection can be found here.

Yet the story of Sixt is also one of a family-controlled and owner-operated company with some “Outsider” elements which has been quite profitable in a competitive market. When reading materials about Sixt, a common theme was something like this:

“They are doing almost too well given the industry they are operating in. Their numbers are great. But it is somewhat difficult to understand why they are so successful. What is their secret sauce, what factors are driving the company?”

In this post, I will try to drill down on this - let’s see if I find some satisfactory answers. As usual, let’s start with some history:

Sixt was launched in 1912 by Martin Sixt with seven cars when actually very few people had cars. The business was a car rental company from the beginning, initially focusing on daytrips for wealthy tourists. In 1927, Martin’s nephew Hans took over and difficult years followed. During WW2, all cars except for one were confiscated by the German army and in 1945 the main facilities in Munich’s Seitzstraße were destroyed by bombs. Still, Hans Sixt carried on with the idea and 1951, “Auto Sixt” was founded

When Erich Sixt (born 1944) took over the company in 1969 from his father Hans, there were about 200 cars and the company was already in expansion mode. It opened branches beyond Munich, in particular at German airports, added trucks and vans to the fleet and started automatic car-rental machines. From the beginning of its expansion, Sixt always positioned itself as a premium supplier (they call it “focused premium straetgy”). Sixt, unlike other car-rental companies, has always invested in its brand and, moreover considered itself a premium brand. This is reflected in offering an overproportionate share of premium-branded cars, but also in them striving to make the customer experience pleasant and comfortable, rather than competing on price. In fact, when do a price-screen for certain cars in tourist markets, Sixt never wins on price.

The company grew and went public in 1986. From then on, the company expanded further using various strategies:

Geographic expansion: From the early 1990s, the company went international, at first in Europe. Sixt took the big step across the pond and into the US as late as 2011. This has resulted in a dramatic rise in revenues, with International now being significantly than Germany.

Leasing Segment: The company also entered the Leasing and Fleet Management markets and the activities were carved out into a separate entity which was long known as “Sixt Leasing”. Sixt Leasing went public in 2015 and was initially majority-held by Sixt, however they have exited completely. The company was renamed to Allane SE and is 92% owned by Hyundai Capital, so it seems to be a squeeze-out candidate if anybody cares about these (I have not been active in this space so far).

Technology opennes and Innovation-driven business models: The third major pillar of the strategy in the 2000s appears to have been the openness to new technologies and trends. This includes the early-adaption of apps/mobile solutions including the MyDriver product (a taxi & chauffeur service), pioneering the car sharing space with DriveNow (a joint venture with BMW) and introducing the concept of “Mobility as a Service” (“MAAS”). The company in 2019 launched its ONE mobility platform, an app which integrates Sixt Rent (car rental), Sixt share (Car sharing) and Sixt ride (ridehailing). It seems like they are making a lot of noise about how techy they are and I am approaching this aspect with some scepticism (relabeling a taxi service as “MAAS” does not make it the latest hot thing), but we will look deeper to see what is happening. Also, the openness and adaptation of the company may very well give them an edge an some respects.

The company is today run by Erich Sixt’s sons, Alexander and Konstantin Sixt (aged 43 and 40) as Co-CEOs which Erich Sixt chairs the supervisory board. There has been some criticism regarding both successors from within the family and Erich Sixt’s immediate transition from CEO to Chairman but with the family owning about 58% of the common (voting) shares, they call the shots here. Having two Co-CEOs is also very uncommon and may lead to fragility in case of disagreements, but it may also mean less key-person risk and more balanced decision making if they manage to work as a team. I find it very impressive that this is just the fourth leadership in a 110-year history.

There is a number of interviews available with Erich Alexander and Konstantin Sixt in both German and English (see here , here or here). Overall, I find them reasonable even though at times a tad too visionary. They make it really clear that they see Sixt as a company with an imperative to grow.

macht an der Spitze der Autovermietung Platz für seine Söhne Alexander (l.) und Konstantin")

Sixt today

So how is Sixt looking today? Let’s take a glance into their Annual Report. The company does a good job breaking down segment revenues by regions (Germany/Europe/US). Note that France and Spain are the largest markets in the Europe segment.

What can be seen is that the internationalization strategy has been of crucial importance for Sixt as they generate about two thirds of their revenues abroad. Also, the US, the biggest market worldwide and a relatively recent expansion step, is generating significant revenues. Sixt claims to have a 41% market share in Germany and a 24% market share in the European coutries it serves directly. The US expansion strategy is centered around gaining and growing a foothold near top US airports.

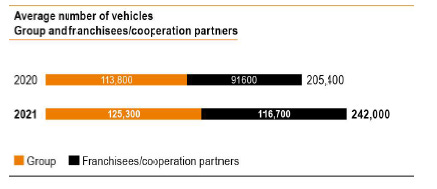

Also, Sixt is present with its own organizations in its more important markets (Germany, Spain, France, Italy, the UK, the US, the Netherlands, Belgium, Austria and a few others). There are about 100 other countries where Sixt cooperates with franchise partners. The combined operations of all franchise partners appears to be roughly as big as for Sixt corporate, yet Sixt generates significantly less revenues here.

I think the franchise strategy is a pretty clever way to advance a future geographic expansion. Besides increasing the size of the network and therefore improving the product offering for its clients, it gives Sixt information and market data on various countries without incurring a lot of cost or consuming much capital. If a country looks attractive, Sixt may scale up and take over the franchise partner. Geographic expansion as a future growth avenue is therefore likely in my view.

Another noteworthy aspect is the close cooperation between Sixt and German premium car brands. 57% of Sixt’s own corporate fleet consists of the Mercedes, Audi and BMW brands. Sixt is therefore certainly a very important showroom window for these companies to get customers familiar with their new models. I am also convinced that the brand focus will result in Sixt achieving very favourable conditions with these three car manufacturers, even though I have not found numbers on it.

Also, while Sixt does a lot of storytelling about its Product Platform, a signature slide of which can be found below, I have not been able to find numbers on the individual segments. If any reader (or the Sixt IR team) is aware of any numbers here, these would be crucial in gaining a better understanding on the more recent initiatives.

I would assume that Sixt Rent still generates the lion’s share of revenues and profits for Sixt. Sixt + and Sixt Truck are logical extensions of Sixt’s business universe but they are quite new and so I doubt they already contribute a lot to the Sixt bottom line.

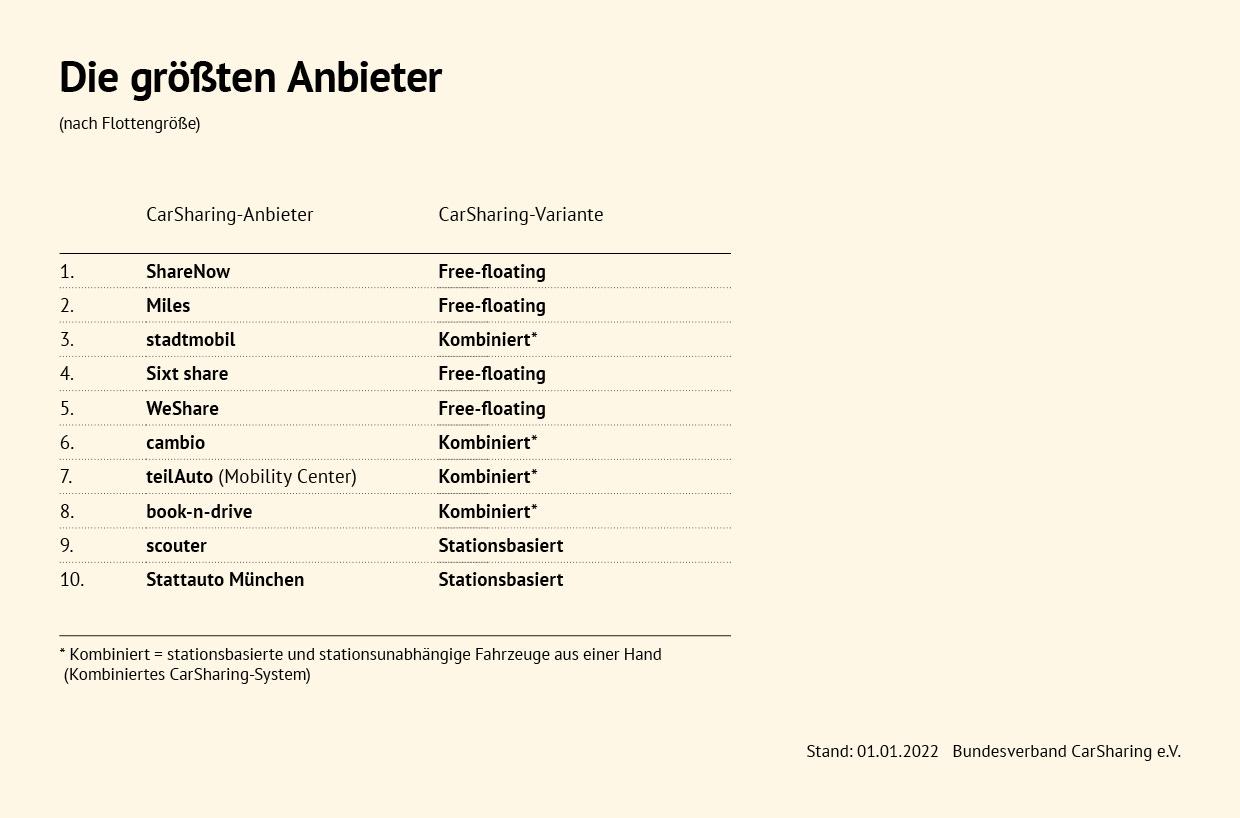

Sixt Share is currently the #4 in Germany’s rapidly growing Car Sharing market . Total revenues for the Carsharing industry in Germany are expected to reach 500mm EUR in 2022 - if Sixt has 10% of this, it would be 50mm EUR. Also, the growing Carshring sector is quite competitive so that I do not expect any significant profits as of now.

Finally, Sixt Ride and Sixt Micro in my understanding are cooperation agreements where Sixt intermediates a customer and receives a fee. This is a profitable, low-risk, low-capital business but I have no visibility how much it already generates. Again, the strategic approach of offering a 360° “Mobility Service” makes sense for a company positioned in the premium segment, even if some services are outsourced but I am lacking some transparency on which element contributes what.

Financials

As usual, TIKR is the source of my financial overview:

Sixt has shown consistent growth and profitability (except for the Corona year 2020). Despite the sale of the Leasing segment, revenues have roughly doubled over 10 years (for a CAGR of 7%).

Both Gross and Operating Margins have improvedin recent years. I think the reasons for this may be (1) carve-out of the lower-margin Leasing Segment, (2) tight cost-management (actual COGS have gone down), (3) pricing tailwinds due to the scarcity of cars in 2021 and 2022, (4) potentially effects from the new segments.

Accordingly, returns on equity, consistently over double-digits anyway have climed to >20% recently. Book Value per Share has risen from 11EUR to 37EUR over 10 years

Leverage/gearing has been stable over the years with the Equity Ratio actually rising a bit while the Interest Coverage seems very comfortable.

Results for the first 9 months of 2022 have been at record levels with the company tracking for 550mm EUR in EBT (2021 442mm)

In Summary, there is not much to be criticized here. The Sixt numbers show a company that is compounding earnings and generating a lot of value for its shareholders. Sixt may currently be overearning a little, given various tailwinds in its markets (strong tourism, strong used-car prices) but the performance anyway looks really strong.

Management / Incentives / Capital Allocation / Share Structure

The Management Board consists of 6 members and is led by the Sixt brothers as Co-CEOs. In addition,there is a CFO, COO, Chief Commercial Officer and Chief Business Officer. In 2021, Sixt paid a total of 13mm EUR to its Management Board including bonuses - a lot of money, but for the Sixt brothers this is peanuts compared to the value of their shareholding or even the dividends they receive. Bonus compensation is linked to an EBT target.

Sixt has a history to pay special remuneration to its staff when times are good (most recently they announced a bonus of 1,700€ per employee here, but it is not the first time). I have always been a fan of motivating people financially so think this is a wise approach to motivate people in times of strong results, high inflation and still tight labour markets.

The company has repeatedly used its capital to build out new business lines, segments and countries from scratch. Sixt considers itself a growth company, so it makes sense to reinvest most of their earnings, in particular where they can generate 15-20% ROEs. Also, the decision to exit Leasing and DriveNow before that shows that they can also part ways with segments that do not fit well anymore. Their share-count has been stable over the last decade with the exception of a small buyback (3% of shares) in 2016. Sixt has been a reliable dividend payer and, prior to Covid (like in 2020) distributed 40-60% of their earnings in most years

Like a number of German Companies, Sixt has a dual share structure with both Common and Preferred Shares being listed on the stock exchange. There are 40.4mm Common Shares and 16.6mm Preferred Shares outstanding, on total around 47mm shares. While only the common shares have voting rights, the preferreds enjoy a dividend of at least 0.05 EUR and 0.02 EUR higher than the common. Note that the Sixt family is owns about 58% of the common shares but no pref shares. Also, the common shares are included in Germany’s MDAX index, so some index funds have to invest in them. These structural factors result both Common and Pref shares being similarly liquid while common shares at the time of writing, trade at a premium of 55% (Share Price 92€ versus 58€). As a retail-size investor, I will have no impact on voting anyway and while I like to close to the family, given the huge discount, pref shares are my intrument of choice.

Valuation

So, here we have a compounding and growing company in a competitive industry, owned and run by the founding family, with modest leverage and 15-20% Returns on Equity which is having a record year. We are expecting an EBITDA of maybe 700mm EUR, EBT of 550mm EUR and Net Income of 400mm EUR for this year. Where should this trade?

Well it does trade at a Market Cap of 3.75 bnEUR and an Enterprise Value of 6bn EUR. This number is basedon a blended common/pref valuations. Yet if you buy the the preffereds and assume they are the same as the commons (which I thinkis fair), you can buy the whole company at a billion less, so 2.7 bn EUR Market cap and just below 5bn EUR EV. So we are talking an EV/EBITDA and a PE of around 7x here. I think these ratios could be at least 50% higher and it would still be reasonable. Also, if the company achieves 400mm in Net Income this year and pays out half that, there will be a 4.35 EUR dividend in the cards, a juicy 7.5% yield on a Pref share price of 58 EUR.

Yes, there may be a recession from which Sixt may suffer, tourism and car prices may weaken or you can find other reasons for short-term weakness. Still, I do think the company has many ingredients to do well going forward.

Summary & Conclusion

Sixt is clearly a highly successful company looking at the hard numbers and facts. Like Autohellas, it is one of those family company success stories where great entrepreneurs with a long time horizon create a terrific company. On my quest to identify the “Secret Sauce” , I found a few factors which the company does differently, where they take an Outsider approach:

They are a premium company in a sector in which most players compete on price.

They have been good at identifying growth avenues in areas adjacent to their original business.

They embrace innovation and technology and try to aggressively use it to their advantage.

They probably have a special and mutally beneficial relationship with German premium OEMs.

Yet, there are still some elements of the company which are somewhat secretive to me and I would like to understand better, in particular the contribution of the new segments on their platform model. If readers can enlighten me further on this, my ears will be wide-open. Any other comments are also appreciated.

Hi Carsten.

Bei Sixt haben wir einen gemeinsamen Interessenschwerpunkt. Wenn interessant für dich, meine Analyse findest du hier ( https://www.youtube.com/watch?v=p3mxTL9xm9I ).

Es hat mich gefreut, dich letzten Freitag Abend ein wenig kennenlernen zu dürfen.

Gruß, Thorbjörn