H1 2022 Portfolio & Performance Review

Thoughts & Updates on Positions

Note: This is not investment advice. Author is long pretty much all of the positions mentioned below and may be biased. Please do your own due diligence.

Augustusville started making investments in March 2022, just early enough to participate in the slide into the bear market. For the total of H1 2022, the portfolio generated a return of -8.6% on a EUR basis. Pretty much everyone except for some energy bulls is down this year, this is not per se a factor to worry.

From an analytical perspective, it is actually great. We can buy shares, pieces of productive businesses much cheaper than before and the companies have not really changed. A downturn in price today inevitably means in increase in future returns. Also, Augustusville still has some dry powder and so we are set up to benefit from cheaper markets.

Still, emotionally, the experience of losing your and your family’s hard-earned money is and will always be a humbling and uncomfortable one.

I am old enough to know that the markets are a system of rising and falling tides and you need to survive the ebbs in order to thrive when the water starts rising.

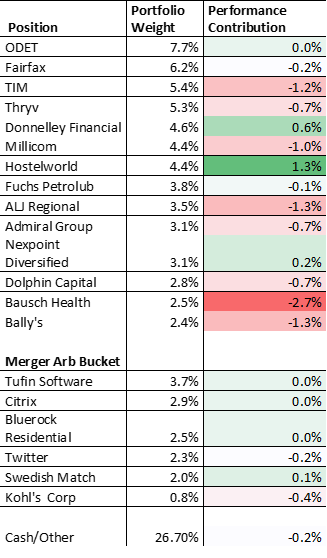

Portfolio:

Compared to my initial portfolio, there are not many changes. I did not sell anything yet added to some existing positions with funding coming in late in the quarter. Also, late in the quarter, I established a “merger arbitrage bucket” and bought a small position in Nexpoint Diversified (NXDT). The portfolio and as of 30 June looks like this:

Some comments on positions - there is quite a bit going on:

Since I invested, Odet bought more shares of Bollore, increasing its share by about 2% (63 to 65%). Given the cross-holding structure (Bollore holds Odet shares), this is in effect a share repurchase and I see it as a positive as Odet and Bollore shares trade at a steep discount to my SOTP calculation and it is a (small) step to simplifying the structure. It is also interesting to see what happens with at the Vivendi level which is trying to buy more/all of Lagardere.

Fairfax agreed to sell the pet insurance segment of its Crum & Foster insurance for 1.4bn USD, about 10% of its market cap. I was aware that pet insurance is an interesting business with high profit potential, yet not of the particular segment within Fairfax. The transaction to me indicates that there is a number of valuable parts in the Fairfax empire. It will be interesting to see what they do with the cash.

Both TIM and Fuchs Petrolub announced share repurchase programs during this quarter. In the case of TIM, this was followed by the decision to not go ahead (for now) with the spin-off of 3LP. For Fuchs, this is the first share buyback program in about 8 years and it is for 6mm shares out of 139mm. TIM received the approval to buy up to 14.4% of its shares and spend up to 100mm PLN.

Millicom (TIGO) went ahead with its expected deeply-discounted rights issue and raised about 740mm USD. I exercised my rights and therebyspend some cash to buy more shares. Tigo also continued the process of buying out some of its local JV partners, this time in Panama. The pending rights issue represented an overhang for the company and I hope that they will now successfully focus on execution and cash generation in their markets. TIGO and Thryv are the next companies I am planning to write up.

Dolphin Capital, a tiny real estate developer in liquidation mode presented a disappointing business update on 30 June. There has not been much progress on the disposal of the three main property assets which are located in Greece and Cyprus. As a consequence, at this point, there is no distribution for shareholders in sight yet. The company still trades at arounf 30% of its NAV, which however has been shrinking and given the interest rate shock, I am not sure about the sale prospects of leisure property in the Mediterrean. Still, I am not yet giving up on Dolphin.

Bally’s (stupidly?) refused a non-binding offer from its biggest shareholder to be acquired for 38USD. In consequence, the share price crashed to 18USD and is now trading around 20 USD. The company, with a market cap of 1.1bn USD implemented a 190mm USD tender offer around current prices and also announced a 3y cash flow projection which includes a continued share repurchase. They also freed up some cash by entering into a 1bn Sale-Leaseback for one of their casinos much of which they will use for building out a new casino in downtown Chicago. If the overall economy collapses badly, Bally’s will probably suffer, but I think it is at this price, it is pretty cheap.

Bausch Health (BHC) spun off and IPO’ed its eye health subsidiary Bausch & Lomb (BLCO). They also stated to not continue the IPO of their Solta unit. Looking at headlines, BHC is really an ugly company. When it was named Valeant it made aggressive acquisitions, pushing debt and stock price until it collapsed. It is still debt-laden (around 20bnUSD versus a market cap of 3bn USD). Xifaxan, the company’s most important product ex BLCO is subject to patentlitigation which might terminate the patent early. I am somehow attracted by this mess - just like John Paulson who was recently appointed chairman. BHC still owns 90% of BLCO, which might be a more stable and modestly levered company and has a market cap of 5.5bn USD. BHC stated its intention to distribute BLCO shares to its shareholders but first needs to reduce its leverage. The credit markets are pricing the BHC’s failure with its debt trading at 50 Cents on the Dollar. So BHC is clear a very risky gamble here.

Special Situation / Merger Arb:

While markets haven been performing poorly, there is now a number of people claiming that “Stocks are dirt-cheap, so let’s load up the truck”. I am not in that camp. While I acknowledge that stocks are generally cheaper than 6 months ago, there is a number of factors preventing me from going all-in yet:

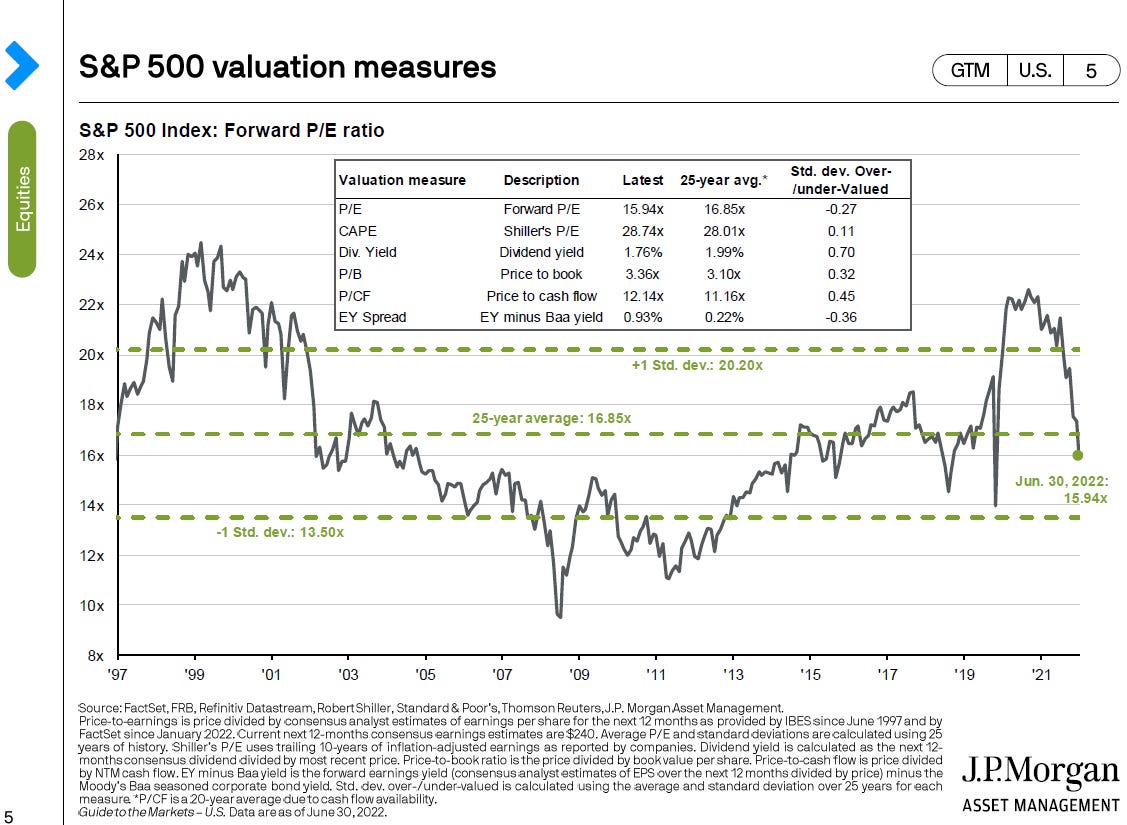

(1) The market was very expensive with stocks being priced at record multiples on record earnings. While multiples have come back to their long term average (not low point), an earnings recession, though likely, is not priced in. Look at JPM’s guide to the markets:

An average multiple on record earnings are not a “screaming buy”, IMHO, in particular since there are real and significant risks to the economy.

(2) I do not see wide-based capitaulation yet: Some of the previously most-hyped pockets of the market, such as crypto, non-profitable tech or fintech are down a lot. Still, there are many people arguing that this is temporary (maybe having the shord pandemic bear market in mind). They may or may not be right. In other segments, I do not see this capitulation yet. People are still “buying the dip” as they got used to that strategy working for 12 years or so.

This is my view and I may be very wrong here. Maybe it is also because it used to be a too early buyer in other situations (look no further than BHC or TIGO). So,what to do? I think it makes sense to nibble some stocks I am convinced of here and, bit by bit and increase my shareholding over time. Also, I may sell some Put Options at low strikes and end up either buying really low or having earned the Put premium.

In addition, I built a merger arbitrage basket for a selection of stocks which are close to being sold. The merger spreads have widened significantly, reflecting the more uncertain environment. As I am mostly looking into deals with a definitive merger agreement signed, I hope for these investments to take care of themselves, i.e. be self-liquidating. Also, the correlation with the general market, while positive, should be limited. Still, there is a number of risks such as a deal not getting approved by shareholders/regulators, a problem with the financing, the purchaser having buyer’s remorse and therefore trying to walk away or cut the price lower. Also, I may not be the most competent person to handicap probabilities and payouts here. So, I went for a basket investment approach as shown above.

Some comments on the Merger Arb Bucket:

Citrix and Tufin Software are almost certain to go thorugh in the next two months or so. Both transactions are funded, shareholders have approved and I am not expecting issues on the remaining process. The same is true for Swedish Match where the tender offer by Philipp Morris International (PMI) has already started. John Hemption by the way thinks that PMI is getting a steal here.

Bluerock Residential (BRG) is an interesting case. The company will be acquired by Blackstone for 24.25 USD. Yet right before the acquisition, there will be a spin-off of Bluerock Homes (BHOM), a REIT expected to have a NAV of 5.65 USD/share. So I could change 26.20 USD against the prospect of 24.25 USD in cash an a share of BHOM. BHOM may become cheaper after the spin (forced selling before trading closer to NAV). Also, I expect for some taxes to become payable upon the merger. Still, I think it is a good deal to park some cash relatively short-term.

The Twitter takeover by Elon Musk is a deal someone might write a book about (Wikipedia is on it already) Musk, somewhat of a wildcard, signed a definitive merger agreement in April to acquire Twitter at 54.20 USD just before the market really collapsed. In the merger agreemnt he waived due diligence on certain topics which he now criticizes very publicy on social media (more precisely, on Twitter), in particular the number of Twitter accounts which are not real people but bots. While Elon runs a powerful media campaign, Twitter is silent working towards fulfilling all the closing conditions which might happen towards late summer. After that, it will be seen if Elon closes per contract, the parties agree a token price cut or this goes to court. While not a lawyer, everything I read points to Twitter havin a strong contract here. So, smallish position in Twitter, if I lose here, I still have a story to tell my grandchildren one day.

Finally, I bought a speculative position in Kohl’s after the non-binding bid by Franchise Group which however collapsed and so I am down 30% on the position. Still, I do think the rationale fora buyer like Franchise Group made sense as Clarkstreetvalue pointed out. The company, while vulnerable to a recession and clearly not the strongest of brands, is still generating cash, yields a 7% dividend, is asset rich and will accelerate its share buyback so I will try to sit this one out.

That concludes my review of positions. Curious to get any feedback. The next post will focus on one company again.

Hey Carsten, just wanted to say great blog and post! I found your blog recently and discovered I own some similar positions. I too believe that companies are not overly cheap at the moment, but I'm finding some interesting special situations like ALJ Regional.

Your opinion to Admiral would be interesting.