Portfolio Holdings - Thryv Holdings, Inc.

Note: This is not investment advice. The author is long shares of the Thryv (THRY), her may buy or sell shares without further notice at any time. Please do not rely on this analysis, it may be erroneous or biased. Please do your own research!

In this article, I continue the series of posts on my company holdings, this time with Thryv, currently my #4 position. For more on Thry, it is worth reading up the Ragnarisapirate blog that spiked my initial interest in the business. There is also an interesting post on VIC on the company

Overview/History:

Thryv is the interesting case of a company consisting of 2 related business in a very different stage of their company life cycles. Having two different segments, yet reporting as one company sometimes blurs the economic reality and potential of a business.

Thryv combines (1) a profitable business in rapid decline, basically a melting icecube, with a (2) growing software/Saas business which should have a further growth runway from here and be about to reach profitability.

(1) Marketing Services: Thryv used to be called Dex Media and its business was the print and online version of the Yellow Pages. It used to be a good business until maybe 25 years ago. Every business was naturally on the yellow pages and paid a fee for this. It was stable, recurring and returns on equity could be enhanced by the use of financial leverage. Unsurprisingly, Dex was LBO’ed yet its fortunes declined when the internet offered local businesses new marketing avenues. Accordingly, Dex went bankrupt and emerged from Chapter 11 in 2016 with former creditors Mudrick Capital, Paulson&Co and GoldenTree as the largest shareholders. At that point, their underlined their digital orientation yet their offering did not appear too cutting-edge:

“Dex Media helps level the playing field and gives these businesses the edge to compete in today’s digital marketplace. Dex Media’s innovative products include social media marketing, digital presence management, online listings, performance tracking programs, and search engine optimization…”

(2) Software as a Service: Still, after emerging, the company managed to build and improve a small business software, Thryv. The idea of Thryv was to have a software for Small Businesses which enables business owners to communicate with their clients, manage schedules, process payments and manage their business from their smartphones. While this may nbot appear to be a revolutionary idea, Thryv was in a good starting position given its Yellow Page history which used to have pretty much all small businesses as clients. Also, Small businesses are certainly not the target clients for titans like Salesforce or Oracle. So Thryv saw a chance to thrive in this space.

What does the business look like today?

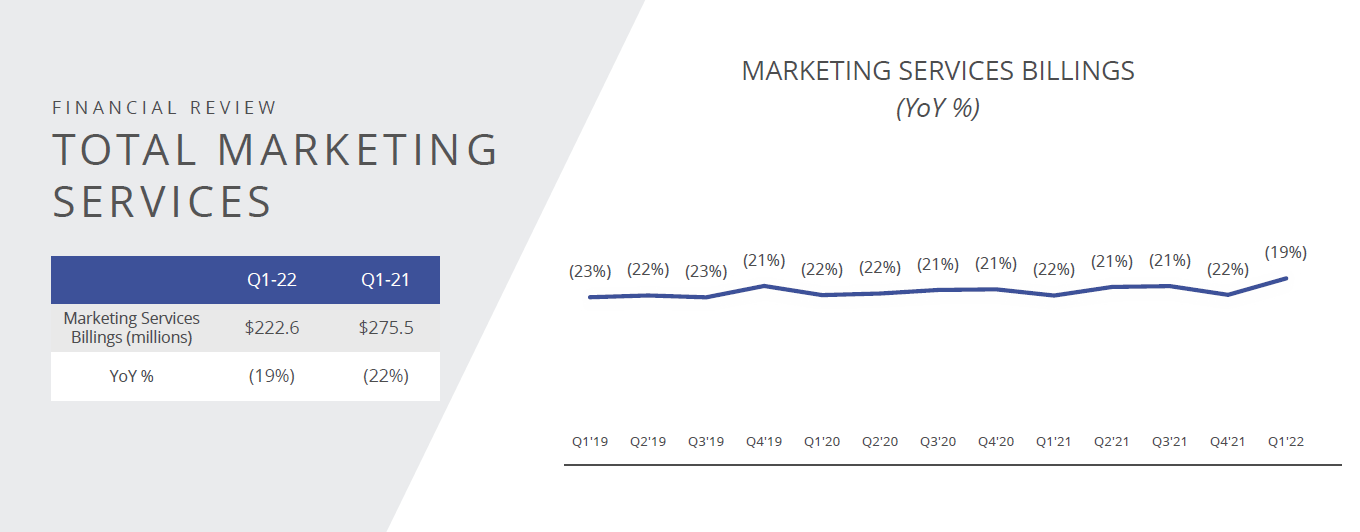

Marketing Services is unsurprisingly a shrinking business. It’s decline in revenues has been constantly tracking around 20% p.a. and Thryv expects for this to continue. What is currently 900mm in Marketing Services revenues is expected to be just 100mm in 10 years. At the same time, they were and expect they will to be able keep their margins relatively high. Thryv explicitly mention that they have a variable cost-structure and are expecting 35% EBITDA margins even at a fraction of current revenue.

Interestingly, recent acquisitions by Thryv were in the Melting Ice Cube Marketing Services segment, including Vivial and Australia’s Sensis . What is the value of the business? I understand it is two-fold. The business, while declining, is still cash generative and that cashflow can be used. Probably more importantly, the Marketing Services clients form the potential client base for the Sofware business to cross-sell and are therefore fueling the company’s growth engine (Thryv are calling this their “zoos” in their investor day presentation).

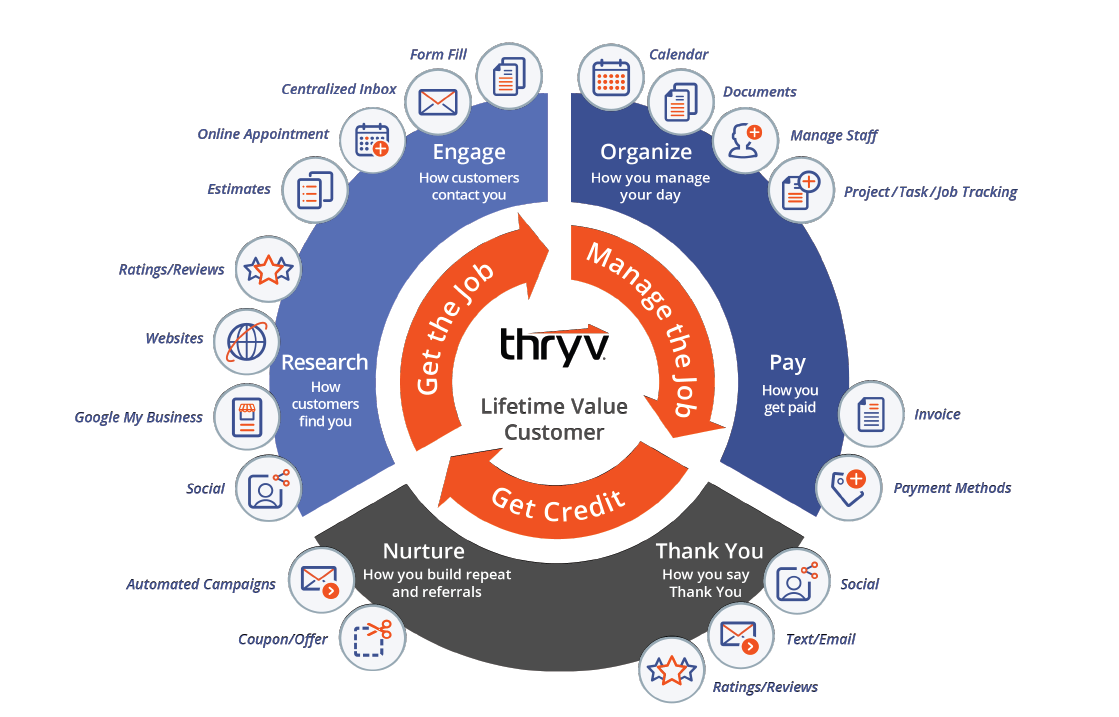

For their cloud-based Software business, they target small and medium businesses with 2-20 employees (they service firms with up 50 employees) and starting from a few hundred thousand USD in revenues. These might be small home improvement, health & wellness, hospitality or law practice businesses. So what does their software offer currently? It offers tools to manage various different aspect of business organization, customer interaction, marketing campaigns and payments.

None of these services are revolutionary or unavailable elsewhere, but I do think that a lean, easy-to-use platform which offers this set of services does have some value to SMBs. Thryv are also constantly working to expand the range of their platform and offer Add-On services, e.g. having started ThryvPay only in 2020 which has been growing nicely. They also launched ThryvHub a tool for franchisors to track their franchise locations.

For H2 2022, they are looking to launch a their “Marketing Center” which will link the CRM feature of Thryv to traffic/analytics and campaign features. Additional features will increase the value of the product ecosystem to clients and may enable Thryv to increase prices. Thryv are also working on a Thryv-branded Visa card.

Thry pricing ranges from 199-500+ USD per month, with ARPU in the SaaS segment reaching 331 USD in 2021. There is competition to Thryv from Salesforce and Hubspot but I understand they are targeting larger clients and their pricing points are higher than for Thryv.

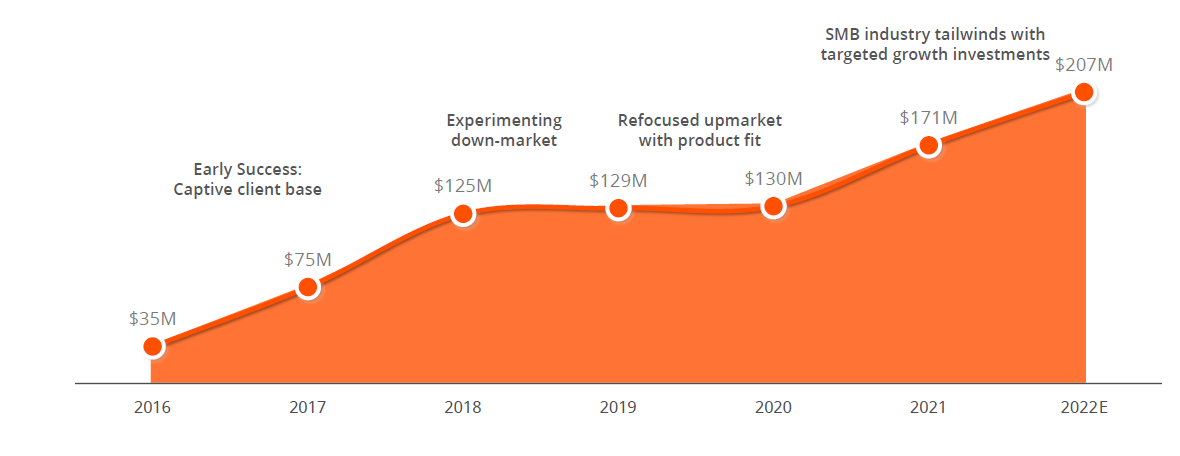

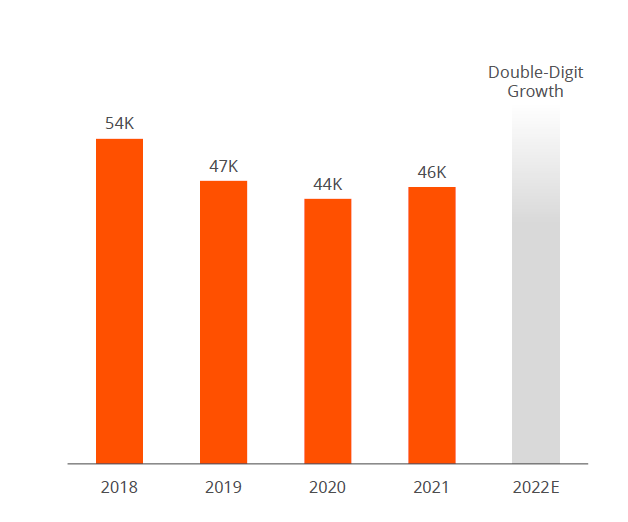

Revenue growth so far has been driven by adding value to the platform and increasing revenues per customer. Revenues over the last six years are up by a factor of 6x which was driven bigher a higher revenue per user while the number of customers has been stagnant over the period of time. When Thryv started, there was no specific client-targeting, they just sold where they could. This has been changing with the share of engaged clients up. It is a critical element to the thesis that the number of customers grows from today.

Thryv are forecasting a double-digit subscriber growth in 2022 (Q1 stands at 47K) and 150K subscribers by 2027. Failure to execute here is a clear risk to the thesis.

Management, Incentives & Shareholders

Thryv is run by Joe Walsh (58) who also owns about 6% of the company and has been in charge since 2014. Walsh has an investment background and was Chairman of Cambium Learning when it was sold to Veritas. Walsh’s base salary is 1.2mm and while is overall package is generous, I believe that he has all the incentives to run Thryv for the shareholders. Given his track record at Cambium, Walsh might also try and sell Thryv to a strategic or PE at some point.

at Thryv, Inc.")

At 17%, Mudrick is still the biggest shareholder of Thryv but they have steadily driven down their shareholding over recent months, creating some overhang for the shares. Jason Mudrick also passed on the Chairman role to Joe Walsh in late 2021 . Paulson and Cerberus are also still on the cap table.

Financials:

Here is an overview over the company financials since emerging from Chapter 11.

A couple of points to note:

Stabilizationof Marketing Services business in 2022 is due to acquisitions and will be temporary. That business has still been cash-generative and permitted a significant debt paydown and share repurchase.

In early 2019, Thryv repurchased about 40% of outstanding shares thorugh in a tender offer. The repurchase for certainly motivated by former creditors looking to exit and happened after the company secured a new debt financing.

There are also warrants for about 5.2mm shares outstanding which have vested and can be conterted at any time at 24.39$/share. These mean a potential slight drag on the equity upside and they expire in August 2023.

Debt mostly consists of a term loan which pay L+850 bps and is due in March 2026. The interest rate is floating from my understanding interest costs rise with rate hikes. Given the expensiveness, debt paydown in my view is a reasonable use of capital and maybe they can also get a cheaper refinancing at some point.

EBITDA on the SaaS business was positive in 2019 and 2020 but turned negative in 2021 and will be negative in 2022. My understandingis that they are investingin that business in order to improve their platform and wind client. I expect that the SaaS could be run profitably today and they are trading profits for growth here. I always prefer to see outrightly profitable businesses but can accept losses for the right reason.

Their target EBITDA margin for the SaaS business alone is 20% by 2027.

Valuation:

So what is it worth?

Thryv bought other Marketing Services companies at 2x-2.5x EBITDA. I will assign a 2.0x multiple here on this year’s EBITDA of 315mm which gives roughly 630mm in enterprise value.

For the SaaS business, I assume that they will do 200mm USD in 5 years and apply a 12X EBITDA multiple to it (revenue multiples are somehow out of fashion these days…) for an EV of 2.4bn in 2027. I will discount this back at 16% p.a. given highrates and some execution risk for a value of 1.142bn of that business today. My valuation is much lower that inthe VIC write-up, given that the tech investing environment has changed quite a lot. Pinning a number on the SaaS business is clearly the biggest challenge in terms of valuation as the market is at a completely different place compared to where it was just months ago and it is not obvious if it was correct then or now. Also, while I am confident that the business will be growing and profitable, the execution of the business plan against their target is still uncertain. On the other hand, management are making it clear that they expect growth beyond their 2027 targets.

Finally, Net Debt stands at 680mm USD. In total, I get an equity value of 1.09 bn (0.63 Marketing Services + 1.14 SaaS - 0.68 Net Debt) USD or roughly 30 USD per shares versus today’s share price of less than 22 USD.

Risks:

What might go wrong for Thryv?

Marketing Services declines faster than expected (20%p.a.): I believe this is unlikely because (1) there is still a need for the product (just saw a new set of Yellow Pages distributed in my German town) . Less people are using ist, but it is not obsolete, (2) Thryv have implemented longer term contracts with their clients (15-18 months rather than 12) to mitigate the effect and (3) they do more acquisitions in that space.

Customer acquisition & SaaS growth does not take off: This is a major risk for me. Thryv are looking to grow revenues by 5x, consisting of >3x subscribers and 1.5x ARPU growth. So they need to grow clients by 25% per year to achieve their goals. Customer growth has been negative until 2020, 5% in 2021 and “double digits” are expected for this year. This is a good trend but 25% p.a. is still very ambitious.

Impact of slowdown/recession: While a recession does not eliminate all activities, marketing expenses might be scaled back and that may have an impact on Thryv. On the other hand, offering a more efficient, Front-to-end marketing/CRM solution my also be a chance during a slowdown and Thryv might actually benefit in the longer-term.

Competition: I personally think that Thryv are in a fairly defensible niche of SMB businesses (2-20 employees) as it does not make a lot of sense for Salesforce or Hubspot to compete here (how would they acquire customers?). Given that Thryv see their growth potential upmarket, they will at some point encounter fiercer competition and it is not clear how this will play out.

Capital allocation mistakes by management: Unlikely. Walsh has been a shrewd capital allocator who just spent 8 years with some of the smarter hedge funds. He is 58 so may well stick around for 7 or 10 years.

Summary:

My portfolio investment Thryv is the case of how the cashflows and client relationsships of a declining business can be used to fuel a new, digital and hopefully profitable business. Thry in my view as a lot of potential to become a secular and profitable growth story in SaaS in which case this might be a home run. Execution, in particular client growth, need to be watched carefully. Long Thryv.

Great post. Somehow one stumbles over the same names.

You mentioned the outstanding options, yet you did not take a claim on equity into account in the Valuation section.

(disclaimer: i do mention options and don't follow through in valuation, too)