Portfolio Holdings - Millicom (TIGO)

The Latam connectivity company that the market has given up on

Note: This is not investment advice. The author is long shares of TIGO at the time of writing and he may sell or buy shares at any time without notice. The author’s views may be biased and his assessments inaccurate. Investing in shares is risky and may result in losing the entire invested capital. Please do not rely on this piece and do your own research.

As my half-year portfolio overview shows, Millicom (Ticker: TIGO) is roughly a 5% position for Augustusville and as announced in the overview, I will share some thoughts on the company. Note that I have been adding to TIGO in July 2022.

Investing in TIGO is clearly an exercise in bottom-fishing. I am showing the 10y chart here in this emerging markets business here which shows how many investors have made most frustrating and humbling experiences with the company. You may find such a chart repulsive or attractive and depending on which camp you are in, finish reading at this point or dive into it.

If you choose to dive, there are more resources on the web, notably a great write-up from the Superfluous Value substack, write-ups on VIC (here and here). For folks rather interested in podcasts, there is a great one from January 2022 with Keith Smith of Bonhoeffer Fund and another one with Mauricio Ramos, the CEO of the company, on the Compounders Podcast .

Company Overview & History:

Millicom is based in Luxembourg and its shares are listed in both Sweden and the US. Millicom International Cellular (TIGO) was set up in 1990 as a combination of various telecommunication assets previously held by IB Kinnevik of Sweden and Millicom Incorporated. It initially conducted its activities in Africa, Asia and Latin America, providing digital and communications services such as mobile, cable, broadband, voice and message services.

Over the years, the company focused its activities more and more on its Latam markets after completing a number of exits first from Asia (last exit in 2011) andthen in Africa (last exit was Tanzania in 2021). On the other hand, the company invested both organically and anorgancially in its Latam markets of like Panama, Guatemala and Nicaragua in recent years.

Kinnevik, a well-known and reputable Swedish tech holding company which used to be invested in HelloFresh, GroupOn, Zalando and others, in 2019 decided to exit 37% its stake in Millicom in a spin-off transaction which at the time created a share overhang and may have contributed to the increased trading volumes and poor share performance in late 2019/early 2020.

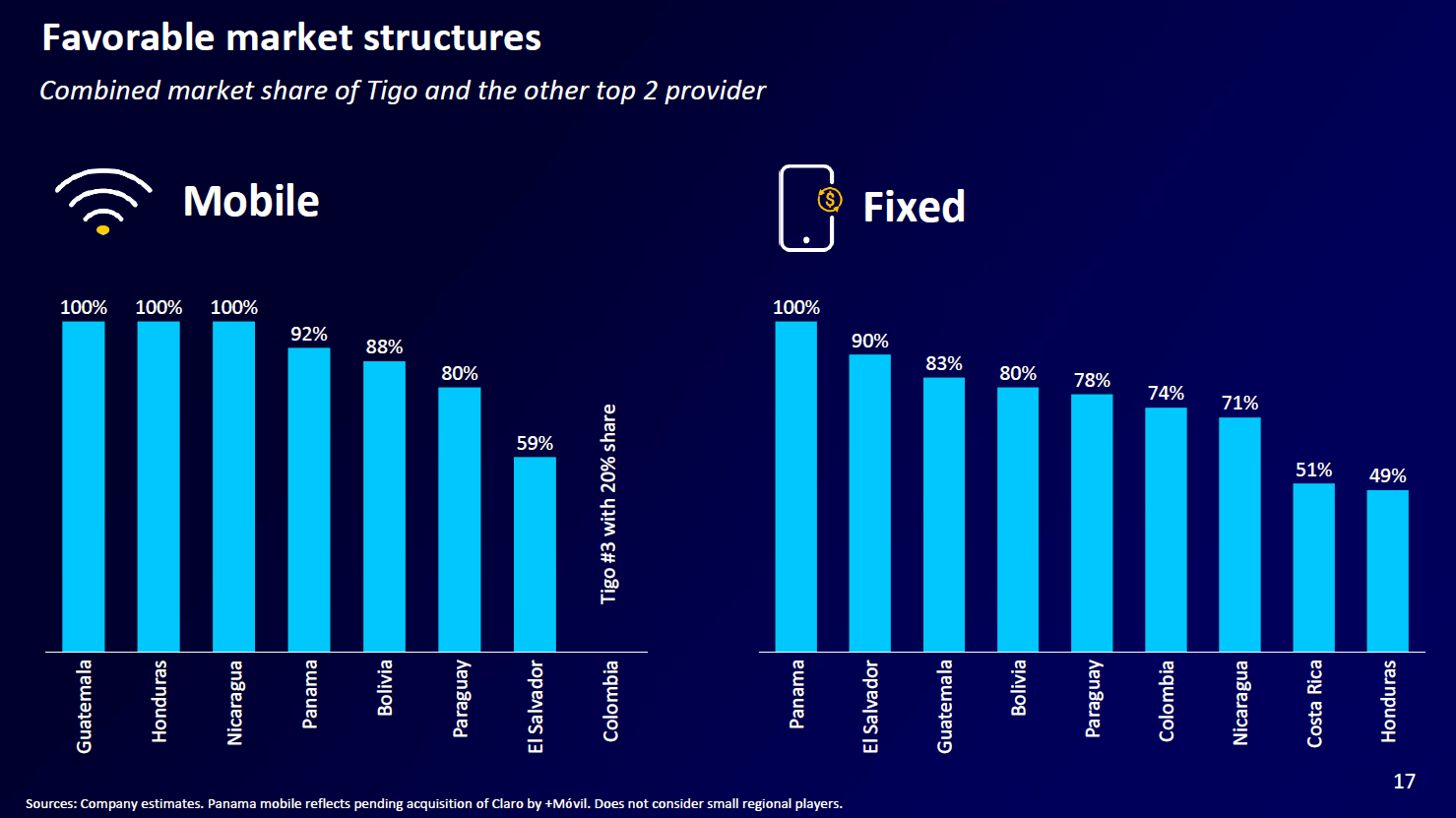

Today, the company is active in 9 Latin American markets. They are not in any of the big markets Mexico or Brazil but rather in medium or smaller countries where they tend to have strong market positions in Mobile, Broadband (BBI) and Pay-TV. One important aspect of the story is that TIGO is encountering limited competition in the markets it operates in with the exception of Colombia.

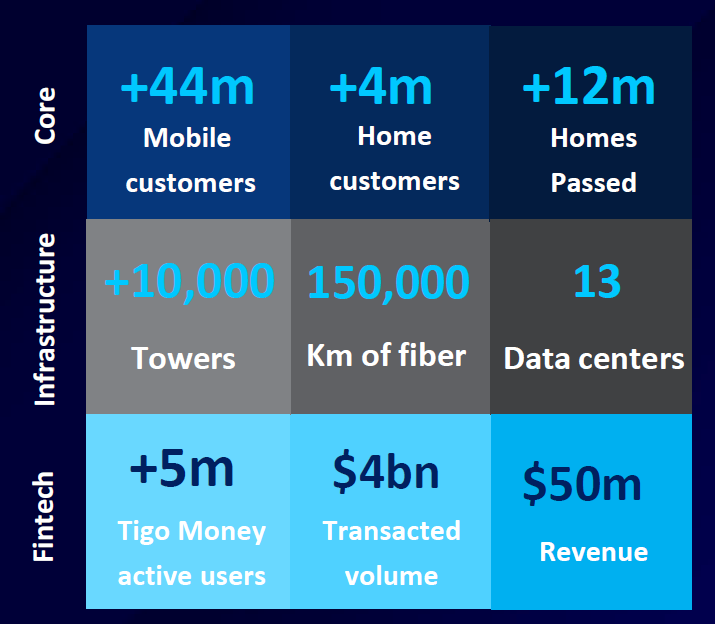

Millicom considers Customer Connectivity” its core business (they have some 44mm mobile and 4mm home/cable customers). Within this business, the fixed line / broadband business is often normally a recurring (subscription) business and thus more stable than mobile which in many cases means prepaid cards.

They also own a lot of the necessary infrastructure, notably 10K+ telecom towers, 150K km of fiber lines and 13 data centers. TIGO is looking seperate and later on sell or monetize its towers in a TowerCo. They also have a payments/fintech business called “Tigo Money” which is currently generates 50mm USD in revenues p.a. and in my view represents a call option to the business:

Country breakdown

Here is an overview of the countries TIGO operates in and their significance for the business (2021 numbers):

Unsurprisingly, these markets are underpenetrated with telecom services, PayTVand banking when compared to the US, creating some opportunities to grow.

Still, when investing in TIGO, you need to get comfortable with country risk, in particular with respect to its biggest markets like Guatemala. Currency risk is an issue here as is a higher vulnerability to political crises or other external shocks (Covid). A beneficial factor in terms of currency stability are the USD remittances by Latinos from the respective countries who are working in the US which stabilize the local economies.

The table above also demontrates how EBITDA margins depend on the competitive situation in the respective markets. In Guatemala, where TIGO is clear market leader, they generate 50% EBITDA margins while these margins in competitive Colombia are closer to 30%. Given the room for market growth, TIGO has been heavily investing in its fiber/cable infrastructure with a focus on increase the number of homes passed, most recently in Bogota .

Also, the EBITDA numbers above include 100% of all regional business while in fact the percentage is lower in some markets. Until recently, there were four Latam markets in which TIGO had no full ownership of its operations:

Guatemala: TIGO owned 55% until late 2021 when TIGO acquired the remaining 45% of the local company Comcel for 2.2bn USD in cash. The transaction has closed and TIGO now owns 100% of its Colombian business.

Panama: TIGO until recently owned 80% of its Panama operations and the seller had an option to sell the remaining 20%. This option was exercised in June 2022, taking the company stake to 100%. The Put Option exercise price has set at 290mm USD, in-line with the original purchase price of the Panama company of 1.46 bn (for 100%) back in 2019

Colombia: In Colombia, TIGO owns 50% + 1 share in the local company, while the remainder is by EPM (Empresas Publicas de Medellin), a public utilities company. In the annual report, TIGO states that EPM intends to sell their share in the business and I would expect for TIGO to have a rightof first offer in the contract.

Honduras: Finally, in Honduras, TIGO owns 67% in a local Joint Venture.

Recent capital allocation / Rights Issue:

TIGO is not that complicated in terms of its business model. It is active in a region some people will not touch. But what really obfuscates the investment case for the company is the changes to the corporate structure and through relentless dealmaking in recent years. I think that right now, the setup of TIGO is much cleaner than it it used to be. Here is why:

The company completely exited Africa. There is only one continent left.

The take-out of the minorities in Guatemala and Panama simplify the business. TIGO can now freely operate in these locations. This will be important when, e.g. it comes to a potential separation of the Tower company. A significant number of the towers is in Guatemala and TIGO can now freely dispose of them without having to ask a minority partner. Also, the take-out of minorities simplifies TIGO’s financial reporting. So far, you had to deal with minorities in profit and equity and JV accounting per the equity method, making it more diffficult to assess “real” sales/EBITDAs/cash flows. This problem has not gone away, but is smaller than it was.

In August 2021 TIGO, having reduced their Net Debt to 2.9x, started a repurchase program for 5% of its share capital. They exercised a buyback of about 1% by early November 2021 when they announced they would buy the remaining equity interest in Guatemala for 2.2bn USD. At this point, TIGO performed a 180° turn, suspended their share repurchase program and they initially assumed a loan to finance the acquisition, also announcing an capital raise in a rights offer.

And I while investors disapproved of the move (and sold the stock), in my view it makes perfect sense. TIGO has been buying an asset of strategic value which it has owned and operated for some time and knows better than anybody else. Also, the price paid at 6.2x EBITDA and 8.2x Operating Cash Flow does not look unreasonable to me.

The rights issue was for 750mm USD and structured as a 7for10 deeply discounted rights issue and the company issued around 70mm new shares at 10.61 USD, increasing the share count from 100mm to 170mm. In this context, you can ask (1) if TIGO really had to raise that much equity or could better have resorted to (more debt instead and (2) if it had do be done in such a deeply discounted issued.

On the first question, TIGO state that they wanted to maintain financial flexibility and not over-leverage. This makes sense to me and they may have had the Panama Option and also a potential deal for the Colombian minorities in mind. The switch from share buyback to risghts issue still feels weird and it can only be explained by them being surprised themselves by the Guatemalan opportunity.

On the second question, I think that the steep dicount and ensuing dilution was crafted in order to benefit insiders. There was an opportunity to oversubscribe on the rights issue and I would not be surpised if insiders did oversubscribe heavily, potentially buying a ton of stock at 10.61 USD. The playbook has been used before in the cable industry (the CEO has a background with Malone / Liberty). While I never like insiders receiving unfair advantages, it has to be said that every shareholder could participate/oversubsrcibe on the rights issue. So this process to me still feels better than some private private placement with the exclusion of subscription rights.

Overall, while the process has been controversial and appears very odd, it seems like sound capital allocation to me.

TIGO has announced they will continue to reduce debt (standing at 3.14x EBITDA in as of 30 June, expected at 3.00x at 31 December) in 2022 and in 2023 look at the potential divestment of their TowerCo, on investor for TIGO Money, further debt reduction (target of 2.0x) and share buybacks. I do not think that any dividends are to be expected.

Management / Incentives

TIGO has been run by CEO Mauricio Ramos (54) since 2015. Prior to this, Ramos was the President of Liberty Global’s Latin America division (now LILAK).

Ramos has been driving the strategic process of TIGO for the last years, including the exit from Africa and entry into today’s Latin American markets. Given his tenure in Liberty Global, we can expect that he knowns the John Malone playbook for shareholder value creation in the cable businesses a focus on cash flows rather than accounting profits, operating at an optimal leverage ratio, and performing clever (sometimes obscure) capital transactions like investments/divestments, spin-offs rights issues. Unlike the share price chart suggets, I do believe that Ramos and the team at Millicom are focused on shareholder value creation.

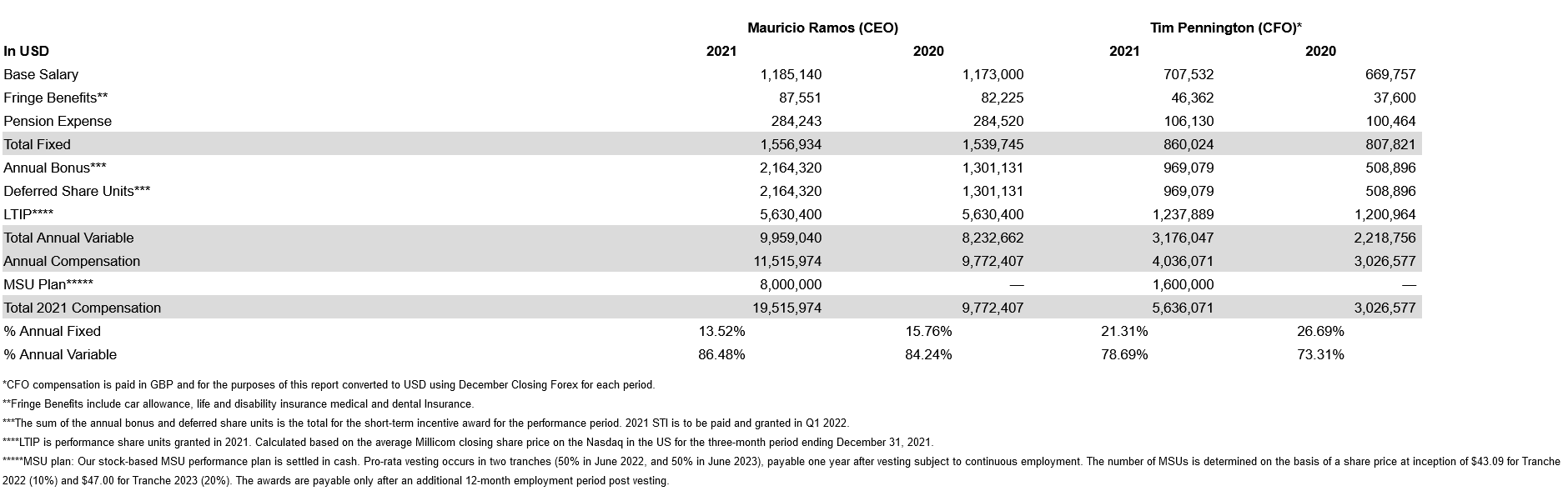

They are also well-incentivized. Millicom pays its top executives a lot of money - the total number for Ramos in 2021 was a stunning 19.5mm USD. The split is quite interesting:

The fixed salary is 1.5mm USD which is not too shocking. The variable compensation is linked to financial metrics (growth in revenue and cash flows) and consumer data (et promoter score /NPS). The variable compensation is split between short-term and long-term where the short-term is in part paid in cash (Annual Bonus) ind in part in shares (Deferred Shares). The Long-Term Incentive Plan (LTIP) is completely share-based. Deferred Shares vest in part after 1,2 and 3 years while LTIP shares only start vesting after 3 years. In addition, the company granted an MSU plan (Market Stock Units) providing a potential cash payment if the stock price reaches a certain level (>40 USD, so currently out of sight) by July 2023. As a result, there is a strong link of executive pay to share performance. Note that the same instruments are used not just for the top executive but for the top 40-50 managers of the firm, including country heads. Also, the top 50 managers at TIGO all have minimum shareholding requirements of at least 50% of their base salaries (and 400% for the CEO).

Overall, I have a good impression of TIGO’s mangement and think they are well-aligned with shareholders.

Financials

Here is an overview of the more recent financials for TIGO. The FY20 and FY21 numbers are pro forma, i.e. adjusted for the transactions which happened recently.

We see a business with steady and stable margins which is growing at mid single digits. If you extrapolate, TIGO might generate 2.3 bn in EBITDA this year. They are guiding for annual capex of 1 bn (excluding acquisitions like Panama) and their interest come may be 550mm (a bit lower in H2 due to recent bridge loan paydown). Also, they might 250mm USD in taxes this year. In total and after Panama, thre may be around 200mm USD in Free Cashflow to shareholders this year. TIGO is in fact guiding for 800mm-1bn in cumulative free cashlow to equity over 2022-24.

The average maturity of their debt is about 6 years at an average rate of 5.8% and the near-term maturities look quite manageable.

Valuation

TIGO trades at 15.24 USD as of this writing for a market cap of 2.6bn USD. Their net financial obligations incl. leases as of 30 June are 7.1bn USD for an enterprive value of 9.7bn USD. So if their EBITDA is around 2.3/2.4 bn USD this year, this is an EV/EBITDA in the 4.1-4.3x area.

Given that TIGO has a clear path to grow revenues from here, margins are stable and the structure has been cleaned up, I do not see why the business cannot command a 6x multiple. Also, I expect for EBITDA to grow from here and will underline that due to leverage a 1x increase in EV means almost a doubling in equity.

There are further interesting datapoints. TIGO just bought 45% of the Guatemala operations at 6.2x EBITDA, valuing Guatemala alone at 5.3bn USD. In Panama they just bought out the minorities for a 1.5bn valuation (5x EBITDA). If these prices hold, the rest of TIGO (7 countries) would go for 3bn USD at current prices.

Also, the TowerCo, data centers and potentially Tigo Money provide some extra value which at some point may be monetized and provide extra value. Overall, TIGO looks really cheap at around 15 USD.

Summary

TIGO is a Latam connectivity business with leading market positions in the 9 Central and South American countries it operates in. Its stock performance has been abysmal due to a series of events that turned investors off (overhang post spin, Coivd, rights issue).

At the same time, the company structure has been cleaned up, its business is much more focused than it was and it has emerged strongly from the crises. TIGO provides an essential service in to its customers in markets with limited competition. It is run by capable and well-incentivized managers and comes at a cheap price.

Augustusville is long TIGO shares.

Thank you for the write up! It seems like a decent opportunity with the future spin-offs.

I didn't realize the management pay is that high for a much smaller company than companies like T and VZ. https://www.fiercewireless.com/special-report/25-highest-paid-execs-wireless-telecom-2019

It makes me wonder about the quality of the board.. why the board thinks the management is worth that much... and what the other C-levels/senior executives are getting paid at. It seems really high for an emerging market country executives. I live in Asia (similar GDP per capita), and the TIGO executives are earning a lot higher comp while running a smaller operation. Maybe I am wrong, but telco companies aren't the most complex industry to run... they have to have someone internal that is capable of running and willing to take a much cheaper compensation package.

It's a difficult industry. If you want something similar maybe even cheaper(EV/EBITDA 3.2x), look no further than Digi Communications (Digi Ro-bbg ticker). Problems here: dual share class, CAPEX intensive. Present in Romania (no 1 in fiber, challenger in mobile), Spain (mobile, data), Italy (small). They just sold Hungarian ops at a very good valuation. Digi was listed in 2017, flat from that point.