Portfolio & Performance H1 2024

Comments on positions and thoughts on contrarianism

Disclaimer: This is not investment advice. The below article is for enntertainment purposes only. Views expressed may be wrong or flawed. The author may own positions in the stocks mentioned and my buy or sell these stocks at any time without prior notification. Please do your own research and do not rely on the below.

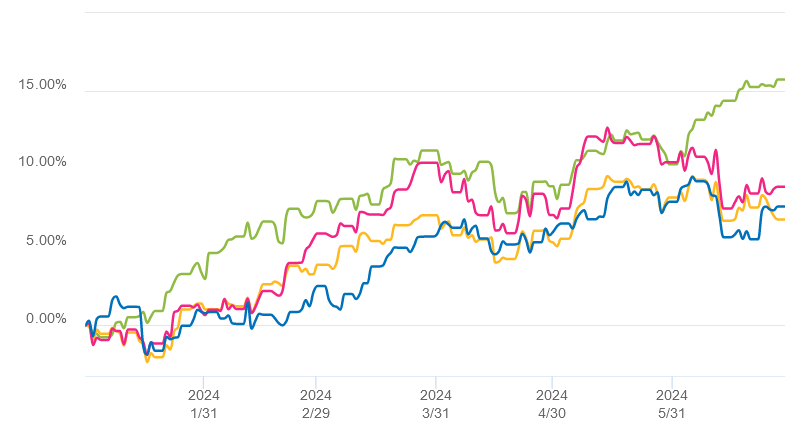

The Augustusville portfolio ended H1 2024 with a performance of +7.6% (gross in EUR). While I consider a satisfactory return at an absolute level, we have been lacking various indices, in particular the ones focused on large-cap tech. We take some solace in the fact that some similarly oriented portfolios run by investors we respect (such as ValueandOpportunity or EmergingValue) have produced comparable returns in H1 of 2024. More importantly, we are not here to play the relative performance derby and we try to not get distracted by short-term performance - and 6 months is clearly short-term.

For those who like nice little graphs, here is a comparison of the H1 at Augustusville (blue) with the DAX (red), DJSTOXX 600 (yellow) and iShares Core MSCI World (green). No worries, we will not start indexing because of this.

What’s new?

The current composition of the portfolio can be found here. We have found market levels quite lofty for some time and, during H1, tried to increase to increase the average quality of my portfolio companies towards firms with a long history of profitability and high returns on capital, but (as we hope) cyclical issues. Positions in companies like Nilorn and AO Johansen were mentioned here before and in H1 we added in Germany, now once again considered the sick man of Europe. While the German economy has been lacklustre and the export-oriented business model has been challenged by what appears to be a new wave of economic nationalism, there is still a number of companies which I expect to do well. Two of them were written up by Valueandopportunity, Amadeus Fire and Hermle . Both companies have long track records of high and rising profits coupled with excellent returns on capital. Both are financed conservatively with moderate debt levels. Also, both have been compounders for 10+ years but their stock price has come under pressure recently for reasons I consider temporary. This has resulted in valuations which, to me appear very attractive:

Clearly, profits may decline for a year or two, but in the long term, say in 7 or 10 years, I expect both companies to be in a better position than they are now. If you are interested, I suggest to read the detailed high-quality write-ups which I have linked above.

I have reiterated that in investing, you do not have to have every good idea by yourself. In fact, today’s online media landscape gives access to the ideas and thought processes of a lot of really smart and capabale people, and this access is often available for free or for relatively little money. Of course, you are responsible for your own decisions and I strongly advice you to not just blindly follow anybody but always have your own thoughts. What I find fascinating is that the more you read/listen to, the more come to see if the writer’s style and process clicks with you. And if that is the case, you can prioritize them higher in your reading list.

One great new source of ideas which came up in H1 2024 is the “Hidden Returns” podcast. The podcast is hosted by Christian Schmidt and Patrick Schmidt (Schmidt is a fairly common name in Germany) and typically features one small-cap idea which is discussed in-depth. These ideas are off-the-beaten track, typically iliiquid micro/nano caps, sometimes with a special situations angle and is held in German. I think the podcast is really high-quality and even though I do not agree with everything discussed and would not invest in every stock pitched, it is a great source of ideas. It was this podcast where I learned of my new portfolio position Supreme Plc, a UK distributor of various products including batteries, vaping products and health/wellness nutrition. In the podcast, Supreme was pitched by Sven Klaß who also did a great write-up. I generally like distribution businesses which often are non-glamorous yet essential and Supreme, since its IPO about 5 years ago combines has been a particularly profitable one, combining (largely external) growth and high capital returns. The stock has run up since pitch (and since I bought), but at 6-7x EBIT still appears attractively priced.

Another addition to the portfolio has been Text SA of Poland. The company, formerly known as LiveChat, offers chat communication software for websites (Livechat product), chatbots for customer service teams (Chatbot product) and Helpdesk, an online ticketing software. Text SA has been a great success since it went public 10 years ago - however, recently the stock price was cut in half:

There has been a debate on whether AI will make Livechat obsolete or whether it will help them. Olivier at ReturnsJourney had a detailed post on it (Paywall). In my view, the speed at which AI takes over the world is overestimated. Text SA has a large and diversified customer base which lets them generate recurring revenues. They have expanded into new products and they have a team which got them to where they are now. So my bet is they will not go away but rather keep on growing. The business is hugely cash-generative and has generated consistent ROICs of 100%+, paid out all of their earnings in dividends and grown at 20%+ over the last 5 years. I was able to buy shares at around 9x EV/EBIT. The stock rallied over the last week when Text posted stronger-than-expected sales growth.

In the “other” bucket of my portfolio, I have a number of smaller special situations positions. These include small positions in risky merger arbitrage in Albertson’s and Capri, some liquidation and odd-lot tender positions. Since the beginning of 2024, I have full access to SSI, a special situations platform which in my view tracks a number of situations really well.

What’s out?

One situation we completely exited was Liquidia. After buying late in 2023 at around 6.30, the biotech company’s share price rallied significantly after a win in its patent case. Ever since, investors are waiting for the company to get their Yutrepia product to market. Liquidia may have much further to run if the commercialization is successful. But until then, it is a loss-making enterprise whose powerful competitor United Therapeutics (UTHR) is doing what they can to delay them. I did not prefer this setup to the above opportunities so I took profits and exited.

We also exited our position in UK life and pension insurer Legal & General. L&G held their capital markets day in June, announced a simplification of their structure and some share buybacks. Is it all good then? Well, I had hoped for more, in particular a larger buybacks and a faster profit acceleration. I am also struggling if I can understand a fairly complex business like L&G which is also covered by a number of sell-side analysts better than other investors. Investing in L&G should not be a disaster from here, given its 9% dividend yield which is more likely to grow than not and supporting the share price. I still opted for other opportunities and sold my share at a level close to my entry, having effectively just pocketed the dividend.

United Internet is a company which we picked up at a point of high pessimism when it traded around 13.30 EUR. Around that time, there was massive uncertainty regarding the buildout of the 5G network by 1&1, one of its two main holdings. While 1&1 is currently still behind its original plans, its has recently caught up and there are signs that its network is growing. Moreover, the German regulator has so far shown mercy with them, probably hoping for a more competitive market while their competition (mainly Deutsche Telekom) keeps on attacking them. The other big holding, Ionos, has been executing well and been rewarded with an increase in share price. I still think United Internet is interesting here, however I could not get myself to add at a current levels in the low 20s and sold out when cash was needed for new positions.

Winners & Losers:

Top performers of Q2 have been Hortico, Supreme, Corecard and Millicom. In the case of Corecard, the rally has been short-lived and the share price has declined again in July.

Hortico, a Polish supplier of horticulture products did catch a bid after reporting strong figures for the seasonally important first quarter. There is some hope that the company is on a growth path again after two years of relatively flat revenue development. After the price increase, Hortico now trades at 6x EV/EBIT and 8x PE, still a modest valuation. Shares are illiquid as this is still a small company with a market cap around 20m EUR.

Millicom (TIGO) currently presents an interesting setup. Operational figures have been improving in recent quarters and the company (market cap of 4.3m USD) is now targeting a Free Cash Flow to Equity of 550m USD for 2024. Moreover, Millicom has been repurchasing shares since December 2023. For some time, Atlas, a company owned by French billionaire Xavier Niel has been a buyer of shares and accumulated a stake just shy of 30%. Just a week ago, Atlas launched a tender offer for all the outstanding shares it does not own yet at a price of 24 USD/share. Given that shares traded just below 24$ and profitability has been improving, the offer is clearly not generous and I would be surprised if Atlas would get the 95% of shares they have been targeting. Moreover, the Independent Bid Committee , formed by the company board, has concluded that the (preliminary) bid significantly undervalues the company, given its prospects. So in my view, it appears likely that the bid price will be hiked while 24 USD might provide a floor. Potentially, other bidders could enter the game. Retrospectively, it turns out that the deeply discounted rights issue two years ago waas a pretty good time to accumulate shares. Insiders back then oversubscibed heavily and we should have done the same.

Interesting developments are taking place at WeConnect, another winner of recent months. In April, the group (market cap of 55m EUR; net cash) announced strong results for 2023 with an EBIT of 10.8m EUR and net income of 9.5m EUR. WeConnect continues to trade dirt-cheap even though the company has managed to grow and generate consistent returns on capital. In late June, WeConnect announced the acquisition of MCA Technology, another IT distributor with a focus on Dell and Lenovo products. With this acquisition, revenues are expected to grow from 264m EUR in 2023 to 400m EUR in 2024, significantly enhancing the scale of the business. If WeConnect kept its Operating Margin from recent years (4%), this could mean a 16m EUR EBIT for 2024. H1 2024 showed a gradual decline in revenues due to a weak June, however the company affirmed its guidance. We remain excited about the prospects of the business.

The biggest negative performance contributor in Q2 was Odet. While there was significant pressure on a number of French stocks, there are also some specific reasons here. The plans for a battery gigafactory raised concerns about capital allocation plans for the group. At the same time, we are waiting for news on the planned Vivendi split into four entities which could unlock significant value. Also UMG has been executing well and remains a high-quality company to own. We used the recent weaknedd to slightly increase our position in Odet.

We also had to digest a poor performance for Sixt. The company has been suffering from lower prices for used cars, in particular EVs which results in worse financials compared to last year. At the same time, there is some reason for scrutiny. The company has invested heavily in the contested US market which is supposed to be the growth engine for the company, but also very competitive. Moreover, there have been complaints about the “authoritarian” leadership of the two Co-CEOs and the role od founder Erich Sixt. For me, Sixt is still an attractive company which I own happily, but these issues are to be considered going forward.

Another drag in H1 was the position in Burford Capital. The provider of litigation finance had become very popular after its court win against Argentina. Maybe not too surprisingly, it has so far not managed to collect its gain and is negotiating how it could be paid. In my view, there is likely to be a settlement at some point. What makes Burford interesting, in my view, is a combination of a first-mover advantage and good track record in a relatively new investment class which is also fairly uncorrelated with the overall market. It is no surprise that returns can be lumpy here, so I just try to stay patient and wait.

Some conceptual thoughts on contrarianism and where to look for investments

Recently, I have been discussing with a few people on where to look for investments. First of all, as a German I do lament that there is such a weak culture of equity investing in our country. Of more than 80 million people in Germany, only about 12m were investors in shares or stock funds. In my view, if a large majority of the society foregoes the (in the long term) most profitable asset class, it makes a country and its citizens poorer and life harder than necessary. Therefore, in my view, a significant challenge for our society is to improve financial literacy and increase the number of investors. In Germany, you are already a contrarian if you even touch shares.

For those who invest, I think that indexing and investing through ETFs is a great choice for 90%+ of people. Index funds provide cheap exposure to a diversified portfolio of leading companies. You can set up savings pland and benefit from the progress of the world technology and economy without having to select shares or understand much about business. Don’t forget that investing is a highly competitive game and a number of people with great brains and other resources participate in it professionally. Even so, 80% of investors do worse by investing actively than the index.

So in my view, active, non-index investing only makes sense if you enjoy the process. This means you have fun analyzing shares, reading news, looking at financial statements and think about industries. Moreover, if you want to play the stock market game successfully, it helps to do things differently. In financial markets, there is oftentimes a predominant narrative that certain assets or asset classes are either invincible or complete failures. More often than not, this narrative can be read on the front pages of leading newspapers. In my view, if you do not index but invest actively, the biggest edge an investor can have, is to deviate from this media-enforeced majority view. This is called contrarianism and it can take various shapes:

"The time to buy is when there's blood in the streets." This quote is attributed to 18th century Baron Rothschild. Warren Buffett, in a less martial style, mentioned that “The best time to be interested is stocks is when nobody else is interested in them”. Essentially, there are gloomy economic times (think September-11, the GFC or the March 2020) when it appears like the world is falling apart and the global economy is facing abyss. In these moments, you are already a contrarian if you invest in any kind of stock while everybody else is pulling their money out and moving into cash or gold. This attitude of contrarian market timing needs courage but may generate huge rewards.

While there is no world crisis every day, there are also other ways to play the contrarian approach. For example, in recent years and so far in 2024, Large Caps have performed significantly better than small caps. This is not the first time this happens - for example there was a similar pattern in the bull market of the late 1990s. Yet, there were periods of small-cap outperformance aswell. However, for many investors who look at recent results, it is now establisehd knowledge that certain large caps cannot lose while small caps are not worth the risk. But there is more: Very small companies, i.e. Micro and Nano Caps are an asset class most investors don’t look at. There is no analyst or press coverage, the companies are often obscure, their products unknown. Many institutional investors are not even allowed to invest here. It is much more likely to be the only or the first one to discover hidden gems in a company. The Hidden Returns Podcast I mentioned above is just about that. I would argue that focusing on these tiny companies in itself is a contrarian strategy, let’s call it Contrarianism by Market Cap

Another way to act as a contrarian is to look at markets/countries which are currently under pressure and/or out-of-fashion. These effects can be short-term due to political turmoil (like the election uncertainty in France over the last three weeks) or longer-term due to structural issues (think Southern Europe in the Euro crisis). In my experience, if you are able to invest in countries everybody makes a point of avoiding or deems univestable, you act as a Country Contrarian and it can be a great edge. At the same time, I make a point of investing in countries with a rule of law, established property rights, a market-based economic system and a democratic political system. Without these foundations, there is too much political risk (with features like expropriation) and your contrarian edge may not take you far.

Similarly, there is can be Sector Contrarianism. It has happened many times that because of the business cycle, regulatory activity or external shocks, entire sectors get hammered. For example, 9-11 was a shock to the entire stock market but even more to airlines and insurance companies. The Covid Crash was much deeper and harsher in tourism and hospitality than in other sectors. If you invested in these sectors in the dark days of the crisis, your recovery potential was much larger than for the general market. It is important of course, to assess whether a certain sector or activity will be permanently impaired. If Covid restrictions had been in place for longer, more companies might have gone out of business. However, in our view it pays to take a step back and not be overly influenced by fears which are based on short-term results.

Finally there can also be Contrarianism on a Company-basis. A number of companies, in particular large ones, may experience a temporary shift in their business success, accompanied by a sometimes dramatic shift in sentiment towards them. Take Microsoft in 2011/2012. Even though the computerization of the world was taking shape and Microsoft was a part of it, the company was unloved. Customers were cursing Windows and Office which also appeared to stagnate to some extent. Growth rates had declined but the company was still growing. The entry into the smartphone business (the Windows Phone) had failed badly and many investors doubted the product and the acquisition strategy. The share traded in the 20s after having traded at 60 at the market top in early 2000, resulting in 10 years of negative returns. Azure was already there but nobody had a clear idea of where the cloud business might go. Still, the business generated a lot of cash, was slowly growing and upheld attractive returns on capital. At the end of 2012, Microsoft could be bought at an EV/EBIT of around 6.5x. Notably, at this point there was no global economic crisis, the USA were a stable country and the software sector as a whole was not struggling. The rest is history - I will just show the chart here:

Why Contrarianism is difficult to implement

In the author’s view, there are two major obstacles to successfully implement a contrarian investment strategy:

It requires a lot of courage: As the word implies, contrariansim means to go against the common wisdom and act against the herd. You will look into coutries, sectors or companies which the majority of analysts and press wither tell you to avoid or completely ignore. You also have to be motivated to look in uncommon places while your friends tell you how easy it is to get rich on NVIDIA or Bitcoin. You will actively have to act against very normal emotions like fear. This is not easy.

It is not to be applied blindly: While this author advocated contrarianism, the concept itself is insufficient. It should always be combined with fundamental analysis. Just buying a stock which has fallen 50 or 80% is probably a bad idea. Many companies in this type of situations may face problems in their businesses which are difficult to fix. More often than not, there will be good reasons for pricing action. So the investor needs to analysze and take a view on whether the business is in terminal decline or we are only observing a temporary problem. Mr. Market may overreact and sometimes get it wrong, but that is not the normal state of the world. So the concept of contrarianism has to be coupled with other tools of business and stock analysis to achieve a conclusive assessment.

also, tigo's independent adv group needed to hire Goldman Sachs+Morgan Stanley AND 2 global law firms !?! cronyism and CYA are better business models than telecom!

alwaysinvertit could have given them a very detailed FV breakdown, but now we will need him to find how much of this 'advice' is buried on the SG&A line item!

Enjoying always to read this blog. Excellent work. I was wondering about the recent drop in share price of Text. It is now trading at very low multiples given the quality of its business assuming the narrative didn’t change. I couldn’t find any specific news that could explain the recent drop in share price and wanted to ask whether some other readers have more information other than their latest press release from 1.10.24