Funkwerk AG - Back on the rails?!

Illiquid hidden champion in train communication systems

Disclaimer: This post is not investment advice. The author owns shares in Funkwerk AG and the views and opinions voiced in the below article may be biased or inaccurate. Shares of the company are illiquid and may be subject to significant volatility. Please do not rely on this piece but do your own due diligence.

I have not posted recently but rather spent time on “quiet” research (and holidays). Also, I tried to build a few positions in micro and nano caps which has been difficult given the market rally. Today, I am writing up one of my latest acquisition, Funkwerk AG, a German “Mittelstand” company which in my views posesses some “Hidden Champion” characteristics. I have been fascinated by the concept of “Hidden Champions”, i.e. companies which are pretty unknown yet dominate a certain (niche) markets or segments internationally, sometimes globally, ever since I read the book by Hermann Simon on it (there has been a recent successor, at least in German, which I have yet to read). The book describes how these companies got there and what they do to differentiate themselves from their competitors. It is an interesting read if you enjoyed “The Outsiders” or books by Bruce Greenwald on competition.

I found Funkwerk when running some quantitative screens which often display cheap yet crappy companies. Whenever a German company pops up which I have not looked at before, my default reaction is to use the German stock almanach which is to be found on the valueandopportunity blog. Here is an extract on Funkwerk from September 2020:

“IPOed into the dot.com boom, the company acquired a lot of other companies and then had to undergo a pretty hard restructuring. Only the last 4-5 years, the company got back on track led by the current CEO.

In 2019, Funkwerk bought a stake in another listed company, Euromicron which became bankrupt a few weeks later. This damaged an otherwise super strong 2019 with EBIT margins >15% and an EBIT increase >+40%.

Despite COvid-19, Funkwerk seems to do well in 2020, as investments into rail is still going strong. The company carries a significant cash balance, which should be a good protection against any future issues.

On the negative side, ~80% of the shares are owned by the Hörmann group which seems to be struggling. So far, no related party issues have arisen, but this needs to be watched.”

This was good enough to get me interested and finally trigger a position and this post.

Quick background on the shares: Funkwerk has 8.1mm shares outstanding. There is only one share class. 78% of the shares are owned by Hörmann Gruppe, so just about 1.7mm shares are in free float. The shares trade at around 22.9 EUR/share as of this writing for a market cap of 185mm EUR. They do not trade on the “standard” regulated German market but the Munich “Freiverkehr” m:access market segment so might be difficult to buy for some readers (IBKR works though). These shares are illiquid and a 4-5% spread is not uncommon, even for limited size.

Overview & History:

Funkwerk is based in Kölleda, in the German state of Thuringia, formerly part of communist East Germany. Funkwerk was started in 1945 as a company for sound reinforcement and hearing aids and shortly thereafter nationalized to become a state company. In 1981, Funkwerk started to produce train radio systems with the GDR state railway company becoming the major customer.

After the reunification, the majority share in Funkwerk was acquired and is still held by Hörmann Gruppe , a holding which today is notably active in Automotive. As of today, Hörmann owns 78% of the Funkwerk shares while the remainder is free-float. Funkwerk has been listed in the German stock market for the last 23 years.

Funkwerk today is Europe’s market leader for train radio systems according to the current European GSM-R standard. They produce and install cab radios and handhelds which are used for voice communication between train driver, control center/signal tower and conductor. Funkwerk also provides systems for the data transmission under GSM-R standard. Funkwerk is also preparing to play a role in the new FRMCS standard which Europe expects to introduce by 2030.

In its second segment, Funkwerk provides solutions for acustic and visual passenger information. Funkwerk’s systems enable rail station operators to display and voice passenger information in real-time and in various languages. This happens based on software which is directly linked to the timetable and traffic data, has access to the train positions and operates almost automatically. Funkwerk provides both software and hardware such as display systems and sound reinforcement for this pupose.

In the third segment, Funkwerk offers offers video systems for CCTV/surveillance and facilty management which in many cases uses IoT technology. In 2017, Funkwerk established a subsidiary focused on IoT.

In 2021, Funkwerk generated about 122mm EUR in total revenue. About two thirds of these revenues were generated in the train radio segment, whereas about one sixth were allocated each to passenger information and video systems. Here is an overview for the last years.

The Train Radio segment has been the big growth driver, notably in 2021. In that year, there were some extraordinary revenues due to a program paid by the German government to support interference resistant train radio (I estimate the effect at around 15-20mm EUR). Geographically, roughly half the revenue is generated in Germany, a third in the EUR ex Germany and the rest in other countries, mostly EFTA.

Funkwerk is not a pure product provider. They also offer installation/implementation services, maintenance, testing and training which may be more stable and less volatile than product revenues and therefore stabilize the overall business of the company. Over the last few years, European countries have stepped up investments in their rail infrastructure as one element of their journey towards a greener traffic system. In my view, this will continue and, as more people use trains, the standards in terms of travel comfort will increase. Funkwerk should benefit from this trend.

For 2022, Funkwerk initially expected lower revenues of 108-115mm EUR. They however acquired Hörmann KN in August and are benefitting from an extension of the government program, so are now forecasting 130mm EUR. Hörmann KN generated on average 30mm EUR in revenues over the last 3 years. Hörmann KN is a supplier of technical infrastructure for trains, a sector related to the Funkwer Train Radio segement. As both companies are part of the same holding group, it is quite likely that Funkwerk know their acquisition target quite well and can form a view on them. I dislike the secretiveness of the transaction (it is related-party and the purchase price has not been disclosed), but strategically, it might make sense. Also, the separate financial statements of Hörmann KN have not been disclosed - I expect the company to be EBIT-positive based on the Hörmann Group Financial Statements.

Also, I hope for more clarity once Funkwerk publishes their annual results.

Financials:

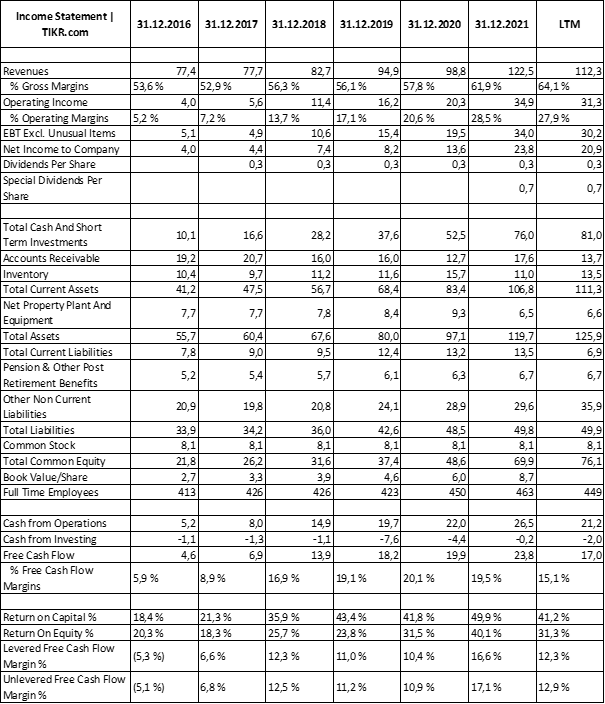

Here are selected items from the financial statements since 2016. It should be noted that Funkwerk was losing money in the years up to 2015. This was however before current management took over and the company’s activities have also changed. As usual, the numbers are an extract from TIKR. Note that Funkwerk accounts and German GAAP standards (according to HGB) which generally takes a conservative assessment on the financial position, but allows smoothing of results in some instances. Here are the main takeaways and they a a major reason for my bullish thesis on Funkwerk.

Over the past 5 years, Funkwerk modestly grew its revenues every year. I described the special effect for 2022 above. More impressively, they improved their margins and profitability by a lot. Gross margins improved by about 10 percentage points, operating margins by about 20 percentage points.

The improved profitability also drove an impressive return on capital which improved from 18% in 2016 (not bad) to more than 40% in the last years. This return on capital was achieved on a bigger capital base than before.

Funkwerk generates in the last two years generatef RoEs >30% despite not only being completely unleverd but also running a net cash position which has grown over the last few years. The company managed to convert their accounting earnings well into free cash flow which is fairly consistent with net income.

Funkwerk’s business did not consume a lot of capex in the last years. They do not capitalize their R&D expenses and beyond that seem to run a capital-light model. The acquisition of Hörmann KN is the only big one they have done over the last few years.

The balance sheet is very conservative and reminds of Japanese companies. Their equity ratio is >60% and almost two thirds of their assets are in cash. For fun, I tried to calculate a Ben Graham style net asset value, resulting in a NCAV of 50mm EUR (~6.20 EUR/share)

From here, we can lazily assume that the dividend distribution in H2 (8.1mm) was balanced by H2 cash generation and still need to account for the Hörmann KN acquisition for an unknown amount. Also, this assumes zero value for the real estate owned by Funkwerk.

The big question is how Funkwerk became so profitable and whether this will last. From about 2015, at the end of a painful restructuring, Funkwerk embark on a strategy of “profitable growth”. If you look at the margin improvements, you will see that (1) gross margins improved. This was driven by the company getting involved in more profitable products. Rather than just selling isolated products, Funkwerk is now selling “system solutions” which connects various hardware components, software, installation, training and maintenance. This and the move to software explains the gross margin improvements. If you look at Funkwerk’s open positions , you will find a number of software vacancies. Also, Funkwerk has tried to standardize their hardware product offerings. (2) Funkwerk improved operating margins by more than gross margins as they also became more efficient. The company worked hard to automate their production process and has the same number of employees as they did 5 years ago, even though revenues are 70% higher.

Investments in rail infrastructure and the ongoing digitalization have been external headwinds for Funkwerk and the company by its own virtue seized these. Today, Funkwerk can act from a position of strength and financial solidity.

Management, Shareholders & Incentives

Funkwerk is run by CEO Kerstin Schreiber (47). She has been on the management board since 2013 and started when the company was financial trouble and undergoing a painful resturcturing which includes the dismissal of many employees. Her background is in finance and she spent her entire career at Funkwerk. Under her leadership, Funkwerk started its path to profitable growth. Kerstin Schreiber is experienced, has been a proven success and at the same time, she is young enough to lead Funkwerk for another 10+ years. I have not found any information regarding Kerstin Schreiber’s share ownership or remuneration.

After Kerstin Schreiber ran Funkwerk on her own for the last few years, Funkwerk in December 2022 appointed a second member to the management board, Dr. Falk Herrmann (52). He is a trained engineer who spent 20 years at Bosch and as CTO will be in charge of the technological aspects of the business. Given the size of the company, I think it is completely adequate to have two management board members.

78% of the Funkwerk shares are held by Hörmann Gruppe, a family-owned industrial holding company founded by Hans Hörmann which operated in 4 segments: Communication (incl. Funkwerk), Automotive (biggest segment), Intralogistics and Engineering. Over the last few years the group performance has been mixed. The group was profitable most of the time, yet margins in the Automotive segment have been fairly slim. Hörmann has a bond outstanding which trades close to par at a yield of roughly 4.5%. Funkwerk has been a significant positive contributor to the group performance. Hörmann’s share in Funkwerk has been stable at 78% for many years and I am not aware of any other intentions. It is a possible scenario for Hörmann to either divest more Funkwerk shares or buy out the publich shareholders in the future, but I have no further insights here.

Capital Allocation and Valuation

Given the significant cash buffer, it is a question of how Funkwerk will spend its money. The company has not issued nor perpurchased share in the last decade. The dividend, cut during the restructuring, was reinstated at a level of 30 Cents/share (total distribution of 2.4mm EUR). In 2022, Funkwerk paid an additional special dividend of 70 Cents for a total of 1 EUR/share. For the last 3 years, Funkwerk had to cope with macro shocks and significant uncertainty following Covid and the Russian war and they managed their balane sheet very cautiously. Looking ahead, I would expect higher ordinary dividends than in the past and a continuation of special dividends if the company continues to perform.

For 2022, Funkwerk expects revenues of 130-135mm EUR and an EBIT of 22-25mm EUR. Take the mid-point of this range and assume a 30% tax rate will mean a bit more than 16mm EUR in net income (not adjusted for cash) or 2 EUR/share. I think that revenues will continue to grow from here and EBIT margins should at least be 20%.

In the last 12 months, without the Hörmann KN acquisition, Funkwerk achieved an EBIT of 30mm. If you take a market cap of 185mm EUR and deduct 65mm in net cash (TIKR reports 81mm, but you can argue to deduct some retirement obligations and other liabilities), EV is 120mm EUR and the trailing EV/EBIT multiple is 4x. The return of positive interest rates may provide a bit of upside too for net cash companies. If Funkwerk invest their 80mm cash pile at 3%, it will be 2.4mm EUR in additional pre-tax income (I would still prefer a capital return…)

There are uncertainties around the acquisition of Hörmann KN - we do not really know how well the business does nor the price paid. Still, the valuation provides significant margin of safety here.

Summary on Funkwerk:

+ Hidden champion in a niche market which might benefit from megatrend tailwinds (decarbonization, digitalisation)

+ Very good profitability, high margins and returns on capital point to strong competitive position and skillful management

+ Strong balance (even too conservative)

+ Experienced and successful leader who can stay on for years

? Limited disclosures (acquisition details, CEO incentives and remuneration) make the company somewhat secretive. An uplisting to a regulated market would improve this.

? Intentions of main shareholder are unclear. There is a risk of related party transactions and Germany is a place where minority shareholders are sometimes taken advanteage of.

? Limited trading liquidity

In summary, I am comfortable enough to allocate a position to Funkwerk which is now part of the Augustusville portfolio.

Any idea why the stock is taking a beating lately? I could not find any news. The whole IR site is very scarse for resources.

I’m a German investor and I have been following this company for 4 years now.

Please allow me to add a few additional comments.

In July 2019 Funkwerk bought a roughly 15 % stake in euromicron, another German listed company back at that time. They invested € 5.8 million, and a few months later the same year, euromicron went into bankruptcy. Kerstin Schreiber back at that time claimed they were deceived by the former euromicron-management. However, if I remember correctly, euromicron was in big trouble at the time of the equity raise, so from a hindsight this move doesn’t look that intelligent. Of course it’s difficult to say who is guilty, but the (rather minor) EUR 5.8 million are lost. This might also explain why Kerstin Schreiber has been waiting 3 more years for the next acquisition. As you conclude correctly, she should know Hörmann KN well as it is another subsidiary of the Hörmann Group.

The stock is trading at a huge discount because of what I call the Hörmann-discount. Hörmann wanted to takeover Funkwerk in total in – I believe it was 2014 – for some Euro 2.x. Speaking as of what we know today, they seem to have been too stingy. As the stock price climbed 15x, it got simply too expensive for them. So they are sticking with the 78 % and have never spoken about their intentions with Funkwerk since 8-9 years now. Neither a move forward (2nd takeover bid), nor a move backward, i.e. selling some shares to increase free-float and to make Funkwerk “capital market viable”. For most institutional investors Funkwerk is simply not investable: Reporting just twice a year, reporting in German-GAAP and not IFRS, No Earnings Calls, no Presentations, no IR-team, no active participation in Equity-Conferences, no mid-term outlook, too little free-float…

If you dig into the annual reports of Hörmann Group itself, you will find that Funkwerk is their only well-running business they have, their diamond so to speak, so maybe they simply don't want to decrease their stake. Excluding the Funkwerk-cash from the Hörmann-Group balance sheet (as they don’t have legal control over this money, but are fully consolidating Funkwerk), you will find that Hörmann is not in the best shape. In 2019 they issued a € 60 million bond which comes due in June 2024. To secure refinancing of the bonds at least 2 years upfront could have led them to sell Hörmann KN to Funkwerk, as this is a legal way to transfer parts of the Funkwerk-cash to Hörmann. However, this is just a speculation. Not disclosing the purchase price to minority shareholders in a 3rd party transaction is indeed a no-go, as minority shareholders have to wait almost 9 months from July 2022 when the transaction was announced until April 2023 when the annual report will be disclosed . I really hope Kerstin Schreiber didn’t overpay for the transaction to the disadvantage of the minority shareholders. In the annual report 2021 they gave a hint that they were planning for € 19 million of investments in 2022, with the major part being capex for the new building and M&A. Let’s hope they have not paid more than € 15 million for Hörmann KN.

While Funkwerk has developed quite well over the years from a fundamental standpoint, the stock trades at the Hörmann-discount. As long as nothing changes, the discount will not dissipate in my view. At the end of the day, stocks follow earnings, and as long as they perform well fundamentally, the stock should trade higher, but keep in mind the Hörmann-discount makes it impossible to being valued fairly.